A huge part of my trading strategy is having a global, no holds barred mindset when it comes to my search for value in the markets. Restricted to companies specifically in the US, one would have trouble finding companies trading at steep discounts to intrinsic value in these US equity markets. With the freedom associated with my global value strategy, I have the option to look to other countries, countries with not so strong ties to the US. These are the companies you wouldn’t easily find in various index funds and ETF’s, and those are the ones that I love to go long on. Remember, when it comes to equity positions, most (not all) of my findings will be in the smaller cap areas, low liquidity, and low volume. This doesn’t worry me, nor should it worry you.

I will admit that in my screening for undervalued companies (which I try to do on a daily basis) I had never come across a company in the Netherlands until today. That company is Aegon NV (AEG). GuruFocus.com defines Aegon’s business as:

Dutch insurer Aegon offers life insurance, corporate pensions, and individual savings and retirement products in a range of markets in Europe, the Americas, and Asia. Through its Transamerica brand, Aegon generates approximately 60% of pretax earnings from the United States. Life insurance and annuities are the two largest contributors to earnings, followed by corporate pensions and individual savings and retirement products.

Before diving in to the company’s fundamentals, it’s important to set out the overall macro framework in which I work with micro data such as stock fundamentals. In my opinion (which, as always, could be wrong and am open to criticism), we are still in the midst of a bull run in US equities that is getting closer to bubble territory due to the overall positive sentiments and indicators globally. With Europe scrambling post Brexit, Venezuela literally up in flames from their socialism experiment, the United States economy remains the “safest” place to invest relative to the rest of the worlds economies. Because of this narrative, I don’t see a tremendous halt in capital flows flowing into the United States, at least for the remainder of this year. With that basic framework in mind, let’s dig into AEG.

Taking a look at their quarterly transcript, I was able to find out that out of every two households in the Netherlands, one of the households is a customer with AEG. That is a market share capture of 50% of the population. Those are incredible numbers.

Digging into Fundamentals

AEG works in a four pronged strategy, each with a specific purpose and objectives. The four prongs of their business are: The Americas, Europe, Asia, and Asset Management.

We know that AEG sells life insurance, pensions, and savings and retirement plans, and we know that most of their earnings (60%) come from the US. Taking a closer look at their balance sheets we can get a better picture of the company’s health. First let’s take a look at big picture trends to see how the company has fared up to this point. Revenues have trended upwards since 2015, along with equity and asset counts. Free cash flows took a major hit from 2016 to 2017, yet still positive. However, net income rose dramatically at the expense of a decrease in operating cash flows. So, we can begin to see the company is using its cash to generate more income for the company, this is a good sign. Now that we have the trend established, let’s see how the most recent quarter reported.

Quarter 3 Report

Corporate earnings increased 20% to 556M Euros. Return on equity increased 1.2[[ to 8.9%, and sales rose 54% to 4.5B Euros. The increase in earnings were driven by, “improved claims experience, higher fee revenue as a result of favorable markets, and lower expenses in the US.” The increase in sales numbers were a result from growth of fee-based businesses. Another main driver of increased earnings in this quarter is due to AEG’s Expense Savings initiative, in which they are on track to save 350 Million Euros by the end of 2018. AEG has increased its earnings the last five consecutive quarters, a great accomplishment.

AEG also reported record gross deposits of 41 billion Euros. The company says this increase is, “primarily driven by exceptionally strong asset management deposits and strong institutional platform sales in the UK.” The company says it remained true to its commitments in each of the four prongs of their business. For the Americas, the company improved their profitability in Life and Health insurance businesses. In Europe, the company positioned its Dutch business to resume its regular dividend payments. In Asia, capital regeneration turned into the black as a result, the company claims, of management decisions and actions. They also rolled out new propositions to help the company transition into the digital revolution. Finally, in the Asset Management sector of their business, the company deepened its presence in existing markets, as well as entered some new markets. They also secured strategic partnerships which will contribute significantly to their bottom line cash flows.

The company is looking for growth areas for new investments heading into the new year and beyond 2018. Most of their findings have led them to refining their search to Asian countries. The company said it wouldn’t chase growth in Asia for the sake of investing in Asia, but it is worth keeping an eye on especially if the Asian economies start to ramp up.

Potential Red Flags

One major potential red flag I see is the overall assumptions to company is placing on the markets returns both in the US and in the UK. For their models, the company is assuming an annual gross equity market return going forward of 8%. I’m not sure we will hit 8%, and if things start contracting, we would be lucky to get annual returns to hit 3-4%. This isn’t as bad as anticipating 10% annual growth, per say, nevertheless it is something to consider if the US fails to hit that mark, which would in turn force the company to adjust its models and pricings heading into 2018 and beyond.

AEG has in place a US micro hedging strategy within the company, in which the company puts an amount of capital into this hedging strategy to make sure they are not over exposed, and are prepared to weather any downturn in the US economy, which eases my nerves a bit.

Some Key Ratios

AEG is trading at 7.25 times earnings, making it better than 85% of the competitors in its industry. Price to book ratio of 0.43 makes it better than 94% of companies in its industry, a number that I love. Price to sales of 0.22 is better than 96% of competitors. It’s also trading at 6.42 times free cash flow, making it better than 64% of its competitors. In terms of all valuation ratios, AEG is at least better than half of its competitors in every category save Shiller PE Ratio.

AEG also sports a 5.00% dividend yield, which isn’t terrible at all. A nice return for holding on to a company whose charts are setting up quite nicely for a horizontal break pattern. Speaking of charts …

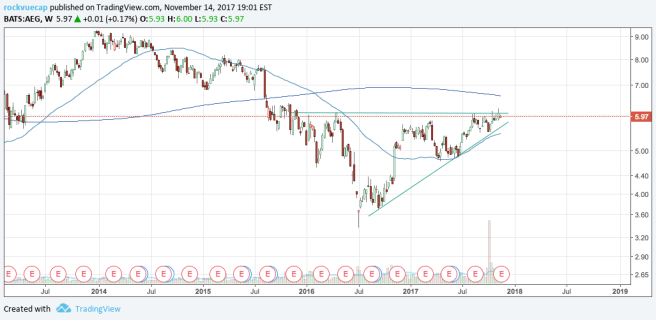

Charting AEG

From the weekly charts, you can see that AEG is forming a year-long right triangle pattern, with price inching closer towards breaking out of that 6.00 – 6.05 range. As a disciple of classical charting principles, I favor horizontal breakouts more than others because of the increased possibility of the trade working out. Notice how I didn’t say probability. I am a huge Peter Brandt disciple, and Peter Brandt always preaches that classical charting doesn’t give a trader probabilities of trades becoming profitable, but rather it gives the trader a possibility of gaining a profit with a trade. This is a huge distinction, and one that I emphasize heavily as well. Peter Brandt is one of the best, if not the best classical chartist on the planet. His words are worth their weight in gold bitcoin.

I am waiting until a clear break above the resistance line on the weekly charts before making an entry. At that point, I would place my stops somewhere close to below the 50MA, which would put it under the ascending part of the triangle, and far enough away to let the trade run its course and give it a chance to be profitable.

As always, please shoot holes in my ideas if you find ways to do so, and don’t hesitate to email with questions.