Estre Ambiental is the largest waste management company in Brazil and Latin America formed via a SPAC offering with Boulevard Acquisition Corp II in December 2017. The company provides collection, transfer, recycling and disposal services to more than 31 million people. Estre (ESTR) is also the sole owner of the largest number of regulated landfills (13) in Brazil with 134 million cubic meters of remaining capacity (15 years worth). To understand the scope of ESTR’s landfill capacity, in 2017 alone, the company handled over 16,600 daily tons of waste. The company is geographically focused on the most densely populated regions in Brazil’s urban markets where they can capture upstream and downstream opportunities for vertical integration. The states in which the company operates represent close to 50% of Brazil’s total population and over 50% of the country’s GDP. Even during the economic downturn of 2014 – 2017, the company managed to churn out 4% CAGR Revenue growth and 29% CAGR Adj. EBITDA growth.

The waste management industry remains highly fragmented in Brazil. ESTR owns 8% of the market share with the remaining top five making up 28% of the market. 47% of the country’s waste is not properly disposed of (read: untapped revenues), and waste tonnage has grown at a consistent 3% CAGR clip since 2008. To go along with the untapped, uncollected waste, the industry will be experiencing regulatory tailwinds going into this summer with the implementation of Brazil’s “National Solid Waste Policy” (which will be discussed later).

ESTR is currently trading near all-time lows after hitting a post-IPO high of $13 back in May. Concerns over leverage, delayed Form 20-F filing, exchange rates, past acquisitions with Boulevard (see AgroFresh), and a Brazilian criminal investigations pump smoke into the potential compounding effects of this durable business with both industry and regulatory tailwinds. However, despite these glaring hiccups, the core business remains solid. The company generates consistent free cash flows, has 30% margins, reduced its debt via Capital Restructuring during the SPAC, and trades at 2x EV/Sales, 4.5x FCF, and 7.7x EV/EBITDA. Management rolled over 100% of its equity into the newly formed company, hired CEO Sergio Pedreiro to initiate a 30% reduction in corporate headcount, and initiated a new results-oriented compensation structure for senior management.

SPAC Overview (Boulevard Acquisition History)

Before diving into the weeds with ESTR, it’s important to understand why the company chose the SPAC route over a traditional IPO, as well as the history of Boulevard Acquisition Corp. Boulevard Acquisition Group is the blank check company formed by Avenue Capital Group. Avenue Capital is a global alternative investment firm founded in 1995 with around $10B AUM. Boulevard Acquisition got its feet wet in the SPAC game by acquiring Dow Chemical’s post-harvest specialty chemicals business AgroFresh. At the time, Boulevard paid close to 9x EBITDA for the company. However, the quarter after Boulevard made the acquisition, AgroFresh reported EBITDA up 26% and revenue up 12%, well above its guidance. AgroFresh remains a high-margin business that produces steady free cash-flows. Since that time, AgroFresh’s share price has stalled and hung roughly around $6. However, Boulevard was able to identify a business in AgroFresh that met the following criteria:

- High-quality Business

- Long runway for growth

- Sustainable competitive advantages

SPACs are great alternatives to entering public markets versus the standard IPO. For instance, a SPAC enables the company going public to have quicker access to public financing than through a traditional IPO. Going public can be expensive when you factor in the “road-shows” that most of these companies rotate through on their way to ringing the opening bell on Wall Street. With the amount of leverage ESTR brought to the table, going public via a SPAC offered the company a chance at both reworking its debt while entering the public markets. SPAC’s have a history of clouded performance. Although the numbers aren’t great, and the historical data isn’t there yet (we only have data going back to around 2004), SPAC’s can be a fertile place to find tremendously undervalued companies and situations.

Brazilian Waste Management Industry Overview

Like I mentioned earlier, the waste management industry in Brazil / Latin America is highly fragmented with many companies filling various aspects of the value chain such as collection, recycling, and landfill disposal. When it comes to collection of waste, no single company holds more than 10% of the industry. Competition is driven by a small amount of larger companies (led by ESTR) as well as smaller, regional companies. To go along with these competitors, companies are also competing with local municipalities’ own trash services. This isn’t as common, but does pose a threat to the free enterprise businesses due to the municipalities abilities to use tax revenues. However, this threat is mitigated as local municipalities can only provide services within their district.

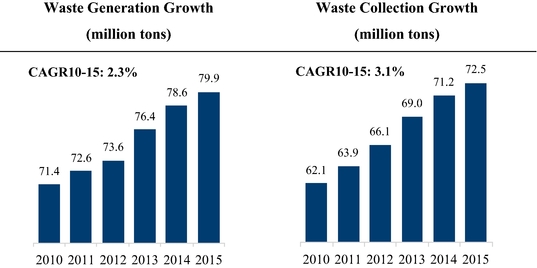

Brazil generated close to 80 million tons of waste in 2015 – 2016, and has average around a 2.2% CAGR since 2010. Brazil is the third highest solid waste generating country behind the United States and China. Waste collection has subsequently increased at a 3.1% CAGR since 2010, collecting 72.5 million tons of waste. The majority of the waste (74.7%) is centralized in two main regions within Brazil: Northeast & Southeast. What’s interesting is that 41% of waste generated was not properly disposed of, and 7.4 million tons of waste remained uncollected. In other words, there’s still 41% waste left to be monetized by these waste management firms, as well as 7.4 million tons ready to be correctly processed and monetized.

Brazilian Regulatory Tailwinds

In 2010 the Brazilian government enacted the “National Solid Waste Policy” (PNRS) in an effort to crack down on the illegal elimination of waste and improper disposal techniques that are going on at the local municipality level. The policy will introduce measures such as the creation of regional waste management authorities, which provides an ability from smaller municipalities to share resources and promote cost reduction programs. The policy also includes tax incentives for energy generated from waste.

The policy states that inappropriate disposal of waste will result in penalties along the lines of warnings, fines, embargoes, and suspension of financing / tax benefits. To go along with these penalties for noncompliance, the government is stepping up its legal regime which will only benefit the waste management industry’s growth trajectory. The new policy requires private sectors to develop waste management plans, making industries like mining, industrials, hospitals, and drug manufactures now on the hook for dealing with their waste in a legal, environmentally safe way. The policy also prohibits the disposal of solid waste into dumps, which will eventually be completely eliminated. This bolsters the demand for landfills (of which ESTR owns the largest number).

The PNRS policy unlocks a huge portion of the waste management industry that was (for lack of a better phrase) under-the-table. By enacting this policy it opens up another 41% of the trash collection industry to be captured by companies that can handle the extra load.

Collections, Recycling, and Landfills

Collections is the first link in the value chain within the industry, putting waste collectors directly in contact with the waste producers. Most of these collection companies are divided between smaller, privately – owned operations and governmental agencies. More than half (52%) of solid waste in Brazil is produced in the Southeast region; cities like Sao Paulo, Rio de Janeiro, etc. 22% is collected in the Northeast Region.

The next step in the value chain is Recycling. Brazil’s waste management collectors work with “recycle co-ops” to sort, compact, and re-sell the recycled waste. Companies such as ESTR house their own recycling operations, but work in tandem with local co-ops as a way of expanding their operations and recycling capabilities while providing incentive for smaller co-ops to work with ESTR. As Brazil’s economy grows, you will see an increase in the amount of recycling taking place, which should provide incremental revenue and margin expansion in waste management businesses recycling operations.

The final link in the value chain is Landfills. Landfills are the most used method of disposing waste in Brazil. Not only are landfills great, durable businesses to operate, but the regulatory environment in Brazil is making it harder for smaller, less known companies to develop new landfills. There are three types of landfills in Brazil, each classified for their varying jobs and quality. The first and highest quality landfill is the Sanitary Landfill (make up 59% of all landfills). Landfills of this caliber are awarded to those with the highest infrastructure standards, as well as meeting the environmental and public safety requirements. Second-tier landfills are called Controlled Landfills (24% of landfills). These landfills have some element of treatment infrastructure in place, but they may or may not be up to code with every environmental or safety requirement. Last and definitely least are Uncontrolled Landfills (17% of landfills). Uncontrolled landfills are, for simplicity, a giant pit of trash with no established infrastructure.

One last thing to note about landfills in Brazil: There are currently 2,255 landfills, of which only 25% are licensed and comply with regulatory and environmental standards. The remaining 75% of “landfills” are open dumps that are considered illegal and will be consolidated / removed under the new regulatory regime.

Projecting Future Solid Waste Growth

If one can project out 3-5 years what the average tonnage of waste might be for Brazil / Latin America, one could then make a rough estimate at the potential growth of the waste management market as a whole. Using conservative estimates, Brazil should increase their waste tonnage around 2-3% a year. This is given the current economic situation. However, if we hypothesized that Brazil’s economy would grow, you could reach a 4 – 4.5% CAGR in waste production growth. Increased production equals increased waste (see: US and China).

Brazil’s waste generation per capita grew at a 5% CAGR clip from 2010 -2015. If GDP per capita continues to grow in Brazil, the International Solid Waste Association projects that average waste per year (on a per capita basis) could reach 470kg per year. This is equivalent to Europe’s current per capita numbers. This increase in per capita waste-per-year would indicate 65% growth in the waste management industry, bringing an additional 40 million tons of waste to market.

Business Overview

Like I mentioned at the beginning, ESTR is the largest waste management company in Brazil and Latin America. It operates 13 landfills with 6 million tons disposed of yearly. The company has over 500 collection services clients, serving over 31 million people. The bulk of the company’s operations are in strategically located, densely populated areas with Brazil that make up 50% of the overall population, as well as 60% of the total GDP. ESTR operates extremely durable businesses. For example, during Brazil’s economic downturn in 2015 and 2016, the country experienced GDP contractions of 3.8% and 3.6% YoY. During that same time, however, ESTR’s service revenues increased 6.9% and 8.1%. The company operates within four business segments: Collections & Cleaning, Landfills, Oil & Gas, and Value Recovery. For the year ended 2017, Collections & Cleaning made up 69.4% of revenues, Landfills filled 30%, and Oil & Gas / Value Recovery each added around 3%.

Collection & Cleaning Services

The company generates revenues through their Collection and cleaning services via household collection from contracts with local municipalities. The company also engages in waste collection for private sector businesses, which adds small revenues compared to its larger household contracts. The company supports its waste collection services with over 980 vehicles (868 are owned outright by ESTR, the remaining are leased). Within collections, most of their revenues are accrued from urban cleaning services such as street sweeping, maintenance of public areas, etc. In fact, ESTR operates the largest urban cleaning service in Brazil for its urban cleaning in the city of Sao Paulo.

Within the public sector, revenues are generated via long-term contracts (typically 3 – 5 years) with local municipalities. ESTR charges based on fees for weight of waste collected, as well as a less commonly used monthly service fee. The majority of these types of contracts have annual price increase clauses that are tied to inflation rates. ESTR also claims that a high number of these contracts are renewed or extended at the end of the scheduled term. The company currently contracts out 12 municipalities, with its longest contract going back to 1995, and the average contact establishment date around 2008-2009.

Commercial & Industrial Collections

ESTR also generates revenues through its contracts with Commercial and Industrial businesses. The company offers private companies the complete waste management chain, from strategic planning to optimizing operational and economic waste efficiency. ESTR meets with individual businesses to figure out their needs, and then prescribes the best method for waste management for their client. This includes diagnostic and waste classification services, as well as supplying waste containers for their customers.

These types of contracts are usually one year in length with options for renewal / negotiation. Pricing is based on estimated weight and time required for the waste management. This segment of the collections business will grow as the Sanitary Policy enacted in 2010 sets forth with its deadline to comply in 2018 – 2020. More and more businesses will now be required to have some sort of waste management plan so regulators know waste isn’t going into illegal dumps or being improperly disposed of. This is important because it keeps the businesses out of fines, and is viewed as a small “insurance like” expense for ESTR’s customers, yet it is almost an unavoidable expense as regulations and penalties tighten up.

Landfill Business

Although the collections segment of their operations accounts for over half of their revenues, the landfill segment is my favorite part of this business’ operations. ESTR increased revenues from $413MR to $455MR during 2015 – 2017. The company owns the largest portfolio of landfills in all of Brazil, and has in its pipeline five more landfills that are set to become operational around 2019 – 2020. In 2017, ESTR’s landfills received a little over 6 million tons of waste. Landfills still the most cost-effective form of disposing waste in Brazil.

Within the landfill segment, 44% of its revenues come from its municipalities contracts, 28% from private & public collection companies, and 27% from larger Commercial and Industrial waste operators. This is important to note as we think about the growing waste management industry as a whole in Brazil. Not only does ESTR own the largest landfill and the largest number of landfills, it is seeking to expand its landfill footprint. Once the regulations kick in and the illegal dumps are disposed of, it creates a huge influx of demand for ESTR’s landfills, even from its competitors. In other words, smaller waste management companies don’t have the landfills in their portfolio and must contract out to ESTR to fulfill their needs. This gives ESTR a tremendous competitive advantage as the industry grows and natural consolidation occurs. The barriers to entry are extremely high when it comes to creating landfills, and are only getting higher with new regulations coming out. First come first serve?

Now with landfills there is the obvious risk of leachate contaminating the water, or chemicals running off into the streets and causing tremendous damage (read: Black Swan Event). ESTR’s landfills are in compliance with international environment policies and standards, and they collect all leachate generated and treat it into reclaimed water for reuse, as well as capturing greenhouse gases to minimize carbon footprint. To date, the company acknowledges they haven’t experienced an operational disruption such as a leakage or contamination with any of their landfill properties. As an added innovation, ESTR is the first company in Brazil to use drones to control and monitor, “the geotechnical parameters concerning the stability of each landfill”. I’m not sure what that means exactly, but the mental image of drones flying over each landfill at the end of the day to check and make sure everything is stable is quite entertaining. Finally, with regards to leachate and contamination problems, each of the company’s landfills is routinely rated highly (from 8.3 – 10.0) on a 1 – 10 scale.

Strategic Locations for Landfills

The company’s landfill focus is in mid-to-large scale landfills (>100 tons per day and total area over 100,000 sq. meters). ESTR’s dumps are located in some of the most densely populated cities in Brazil (Sao Paulo being the most densely populated state in the country). In the Northeastern region, the company believes its landfills are positioned in cities that are both experiencing tremendous economic growth as well as a long runway for continued growth, further increasing its ability to capture larger market share.

The company’s properties have long shelf lives remaining, with only one landfill between 3- 5 years left in capacity. Every remaining landfills has at least five years of operational ability left. That’s at least five years of stable revenues from landfills with increased waste tonnage projected. The average remaining life span for its 13 landfills is 16.07 years.

Revenues and Customers

The company generates revenues from its landfills via disposal and tipping fees based on type of waste as well as weight of waste being disposed. Standard contracts are between 1 – 3 years in length with renewable agreements at the end of each contract and annual price adjustments based on inflation. The customers are similar to that of its collection and disposal clients; citizens, Commercial and Industrial clients, as well as local municipalities.

ESTR is the clear leader in landfills within the waste management industry, and will most likely make up for a greater percentage of total revenues as the company grows and consolidates the industry via acquisitions. Landfills remain the highest margin business for ESTR with close to 50% gross margins and 37% net income margin. With increased regulatory crackdown, as well as countless amounts of red-tape to build new landfills, it blocks out smaller waste management companies from dipping their hands into the landfill revenue pot.

Oil & Gas and Value Recovery

The last two segments of ESTR’s operations represent the smallest fraction of total revenues generated. The Oil & Gas (OG) segment of their operations provides on and off-site biological remediation of soil that has been contaminated with oil. Through its segment, the company provides services in several sites, transfers the contaminated soil to their biopile facilities, and takes it through a “bioventing” process. This isn’t pertinent to the sustained growth potential of the business, so I won’t spend too much time on the details. OG accounted for 4.5% of revenues in 2016 and 1.9% in 2017. ESTR works with (basically) one customer in its OG business, Petrobras, which accounted for 83% of its OG revenues in 2017.

The last segment of their business operations is Value Recovery. Simply stated, value recovery is the use of environment “best practices” in order to create alternative energy, recycle materials into reuseables, and the trading of carbon credits. Although this is one of the smallest parts of their business, it’s actually pretty interesting. Let’s take Landfill Gas-to-Energy for example. The company has a ton of naturally produced methane in their landfills from the waste collected, and through the use of drains and filters, turns the methane into reusable and sustainable alternative forms of energy. By doing this the company generates tax benefits, which help squeeze out incremental margin from its competitors that don’t have the capacity to do the same.

In fact, ESTR has been generating electricity from its landfills since 2014. The company currently operates two gas-to-energy facilities with around 14MW of capacity. To give you an idea of the tax benefits that are being generated, the company sold 38,811MWh in 2015, 49,081MWh in 2016, and 82,005MWh in 2017. Along with their 14MW capacity, the company secured approval for development of five new gas-to-energy facilities, opening up another 46MW of potential capacity. It’s important to know that although this act of selling alternative energy isn’t a main driver of revenues, it does provide tax relief for the overall business, which is an advantage that not many (if any) of its competitors enjoy. Using rough estimates of 80MW power from the company’s already existing landfill portfolio, and if the company is able to charge around $220 Reals / MWh, it would translate into $126M Real per year in additional revenue with very little additional operating costs.

Competition

Speaking of competitors, ESTR’s main competition within its collection and cleaning services are from Solvi, Vital, Marquise, Ambipar, Sustentare, Constroeste, and Seleta. ESTR is the largest out of all its closest competition, servicing the most households (double Solvi’s 14M people served). Most of its competitors are private enterprises, which give ESTR an ample opportunity for consolidation as the industry grows and rolls up. My efforts to find comps for these companies was tough as most of them are private enterprises, and only one of the company’s had an annual report that wasn’t in Portuguese, and to boot, most of these companies websites were purely in foreign languages (Google Translate only goes so far!)

However, if we pan over to the US’ global waste management industry, we see that industry averages are much higher than ESTR’s current valuation. In the US, P/FCF for the industry averages close to 20x. EV/EBITDA industry average is 13x. All of these make ESTR (on paper) seem relatively cheap given its 4.5x FCF and 7x EV/EBITDA.

In fact, there are quite a few parallels between the current state of the Brazilian waste management industry and the waste management industry in the United States during the late 60’s through the 80’s. 1965 the US enacted the Solid Waste Disposal Act, a policy very similar to the one Brazil enacted in 2010. Five years later the US released the Resource Recovery Act. This act is important because it made open dumping illegal. What Brazil has done is effectively rolled up these two US policies into one with the PNRS. By the late 1980’s the US reduced improper destination of waste from 21% to 0%. During the same time frame the US consolidated the number of landfills from 7,924 in 1988 to 1,724 in 2006. If Brazil follows remotely the pattern of the United States, ESTR comes out on top for sure in the landfill space, and is a strong candidate to capture most of the new waste collected.

Debt Restructuring

One of the major clouds surrounding ESTR is its leverage–better said–its perceived over-leverage. Before its transaction with Boulevard, ESTR had Net Financial Leverage of 4.3x. Back in August of 2017, the company entered into a binding facility commitment letter with its creditors to negotiate its debt burden. Both parties came to terms that provided a prepayment of $200 US Million, a partial debt write-down, and the restructuring of its existing debentures. After closing on the agreement, ESTR negotiated a prepayment of $110.6 US Million in cash. Upon receipt of the prepayment, the creditors then granted the company a reduction to 25% of the prepaid amount. This restructuring greatly reduced the debt burden while increasing the company’s cash on hand.

The refinanced debt structure includes interest rate of CDI plus 2.0% per annum, with payments spread semi-annually in 11 installments, all of which starts after a three-year grace period (two years remaining). All of the remaining $1.06B Real is denominated in Brazilian Reals. Now, in order to keep this refinanced deal affirmative, the company agreed to semi-annual measurements that way its creditors know the company is still in good standing. For example, ESTR has to have a Net Debt / EBITDA ratio of at least 4.0x or lower by December 2018 (right now it is on pace to hit that, currently sitting at 3.3x). After hitting that mark, the company must have an annual Net Debt / EBITDA of 3.5x or less (again, under that mark as well given current financials). Finally, for three consecutive semi-annual periods starting in 2019, the company Net Debt / EBITDA ratio must be at least 3.0x or lower.

Given their leverage, the company is subject to interest rate risk (which will be discussed further). By doing a sensitivity test of their loans and financing, the company forecasted various scenarios in which interest rates would flow: decrease by 50%, decrease by 25%, the probable rate, and then increases of both 25 and 50%. If interest rates were to decrease by 50%, the company’s net financial liabilities would increase by around $72M Real. Subsequently, if interest rates were to rise by 50%, the company’s net financial cost would be around $72M Real. In the probable interest rate scenario, the company is facing a probable net financial cost of $144M Real. The debentures Amortization Schedule is very much back loaded, with the bulk of the payments being paid in 2025 ($784M Real). To give an idea on the debt burden the company will face for its debentures over the next four years: $71M Real in 2020, $143M Real in 2021, $143M Real in 2022, and $143M Real in 2023.

The Jockey Running The Show

The company shifted gears dramatically in 2015 after being pulled into a criminal investigation (see details in the Risks section of the write-up), cleaned house, and hired Sergio Pedreiro to do the job. Before joining ESTR, Pedreiro was CFO of America Latina Logistica (from 2002 – 2008). The company is the largest publicly traded cargo railroad in Brazil. After turning that company into the largest in its industry, Pedreiro set his sights on the US, becoming CFO of Coty, the global beauty product company with $8B in annual revenues. After that, Pedreiro served on the board of directors for Advanced Disposal Inc., a US based waste management company that sported $1.4B in annual revenues.

Sergio is passionate about creating a culture of professionalism and result-driven performance. In an interview with Waste360.com, Pedreiro says (emphasis mine), “The company was founded by one individual back in 1999, and it has never been family owned or operated. We have a culture that’s obsessed with professional excellence. If you look at our growth in terms of top line and margins, you will see that we’re ahead of our competitors in Brazil in terms of both the culture and the performance of the company.”

Pedreiro has an impressive resume to his name, which helps build confidence in his ability to permanently change the company culture for the better, get past the criminal investigation, and produce consistent compounding capital returns.

Looking at Financials

Starting with the income statement, ESTR increased top line revenues from 2014 – 2017 from $1.2B Real – $1.36B Real. The company increased gross profit from $351M Real to $411M Real (both increased revenues and decreased cost of operations drove increase). The company turned profitable in 2017 recognizing net income of $52.3M Real which translated to $0.96 Real EPS.

What’s interesting to note when digging into the income statement a bit further is that Landfills and Collections segments had almost identical gross profit even though Collections accounted for $928M Real in total revenues. Collections is a CapEx heavy business with constant maintenance on every vehicle in their fleet, as well as increased labor costs and variable fuel costs. In fact, if you keep going down the income statement, you’ll see that Collections and Cleaning services accounted for a net income of merely $24.9M Real where the landfill business generated $170M Real from its gross profit figure of $196M Real. Most of the reduction in Collections net income is due to increased finance costs. If you go back to 2016, net income from the Collections business was $168.1M Real. The company is cutting costs, however, with cost of services decreasing from $1.02B Real in 2016 to $953M Real in 2017 (closer in line with their 2015 number).

Moving on to the balance sheet, the company sports $84M Real in Cash and marketable securities and $689M Real in PPE, with total assets reaching $2.3B Real. With regards to liabilities, the company recognizes the $1.06B in debentures for non-currents, with another $371M Real in loans and financing. Labor costs rose over the last two years with the company paying close to $120M Real for labor, up from the previous year’s number of $106M Real.

The company is cash flow positive, and has been for the last four years, sporting $243M Real in cash from operations for 2017. That figure is up from $213M Real in 2016 and $235M Real in 2015. The bulk of the increase in cash from operations from 2016 – 2017 was due to increased collections on accounts receivable.

Projecting Revenues, Earnings, and Fair Value Range

According to its 20-F, the company is forecasting net revenues of $1.63B Real ($404M USD), EBITDA of $462M Real ($115M USD) for an EBITDA margin of 28% for 2018 Year End. It’s important to note that the company is projecting those figures while taking the following into consideration:

- It’s not assuming any positive changes in Brazil’s economic condition.

- It is not assuming any acquisitions.

- Not assuming improvements that management believes will take place due to restructuring of debt.

- Assuming 100% of its contracts will be renewed.

- Assumes that ESTR signs only 29% of its pending contracts and pipeline of potential contracts (the company historically experiences 75% success rate on new bids).

Bringing that down to EPS, the company expects to earn $0.42USD in 2018 and $0.58USD in 2019. This would represent P/E ratios of 16.5x in 2018 and 12.0x in 2019. If the company can continue to churn out around 4% CAGR revenue growth with 20%+ EBITDA growth hitting those earnings numbers shouldn’t be completely out of reach.

Finding a Fair Value Range

The company is currently trading at 7.7x EV/EBITDA. This is a 25% discount to the average multiple that US waste management companies garner, 10.3x EV/EBITDA. At its current multiple of 7.7x we get an Enterprise Value of $790M USD. Let’s assume that ESTR worsens on top-line revenue, fails to grow, and is -3% on average for the next three years. Averaging -3% CAGR revenue growth gets us to $347M USD. If we take 29% EBITDA margins we get $101MM EBITDA. Taking our multiple this gives us an EV of $777M USD. Adding back our $25M USD in cash and subtracting the $453M USD in debt we get a Common equity value of $349.7M USD. Divide that by 51m shares and we get $6.86/share.

If we look out over the next three years and assume a 4% CAGR in top line revenues, it puts revenues at $461M USD. Taking the historical average EBITDA margin of around 28%, we get $129M USD in EBITDA. Applying the same 7.7x multiple we get an Enterprise Value of $994M USD. Holding cash consistent we add in another $25M and decrease our debt of $453M. This gives us a Value of Common Equity of $521M USD, divide that by 51M shares outstanding and you have a fair range of around $10.25, a near 50% increase from current share price.

Finally, to find the upper range, we’re going to apply the average multiple for the US Waste Management industry to ESTR’s current EBITDA of $102.7M USD. This gives us an Enterprise Value of $1.063B USD. Adding back in our cash and subtracting our debt, it gives us a Value of Common Equity of around $635M USD. Divide by 51M shares outstanding and you get around $12.50 per share, an increase of nearly 77% from current trading prices.

| Model | |||

| Low | Mid | High | |

| Enterprise Value | 777 | 994 | 1,063 |

| (+) Cash & Equivalents | 25 | 25 | 25 |

| (+) Investments & Other | 0 | 0 | 0 |

| (-) Debt | 453 | 453 | 453 |

| (-) Other Liabilities | 0 | 0 | 0 |

| (-) Preferred Stock | 0 | 0 | 0 |

| (-) Other | 0 | 0 | 0 |

| Value of Common Equity | 349.7 | 566 | 635 |

| (/) Shares Outstanding | 51 | 51 | 51 |

| Implied Stock Price | 6.86 | 11.10 | 12.46 |

| Upside / (Downside) | -5.30% | 63% | 77.8% |

This is a rough range of potential price outcomes given different scenarios, and remember, there is a non-zero chance that ESTR could go to $0 per share given its leverage position. We gave these scenarios with debt staying steady, if we decrease the debt burden, it elevates the upside tremendously.

The Warrants

To go along with the regular equity, the company also issued warrants on a 1-for-1 basis with a strike price of $11.50. Given the 1-for-1 nature of the warrants, it presents an interesting option for investment into ESTR. Warrants (by nature of being derivatives of the underlying) tend to swing more drastically in price than if one were to buy the regular equity. However, your risk/reward profile is asymmetrically in better favor than the straight equity. Warrants are currently trading for $0.48, with a 52 week high of $1.03 and a low of $0.33.

Risks

There are a myriad of risks that pertain to this investment, I will try to address all of the risks that are most pertinent to inflicting damage to the company’s compounding abilities. These risks are: Interest Rate, Recent Criminal Investigation, Overall Debt Burden, and Loss of Major Contracts.

Risk #1 – Interest Rate Risk

The company negotiates contracts with inflated adjustment measurements to protect themselves against violent swings in that regard, however, I am more worried about the risk for their debt. Since nearly all of ESTR’s debt burden is linked to floating interest rates in Reals, any rise in interest rates would increase the cost of their financing exponentially. Now, this risk will potentially be mitigated as the company pays down its debt and reduces its overall leverage (goal is 2.9x Net Debt / EBITDA by 2020). Further increases in interest rates could mean operating losses for the company as cost of liabilities rise above revenue generated from operations. If this were the case, the company would be faced with either selling off assets (they use landfills, vehicles, and land as collateral for their debentures) or raising more equity via share offering or debt financing in order to continue operations.

Brazil’s economy is growing and projected to continue to grow to the clip of potentially 2 – 3% a year; this is after three years of negative GDP growth. If GDP continues to grow the government might loosen interest rates, make capital cheaper to borrow in order to encourage growth and spending. The same argument can be made for when the economy gets close to overheating, and then higher interest rates are installed. I hate predicting where macro interest rates will fall, but at least this gives us two potential models to work from.

Risk #2 – Criminal Investigation

It goes without saying that criminal investigations are never a good thing for a business. Even if the company is found clean and free, being swept into an investigation is bad press and can suppress demand for investment into the company long after the dust settles. ESTR has been a subject of allegations and investigations of misconduct, specifically relating to documentation regarding ESTR’s transactions with certain identified suppliers. The investigation is due to accusations of bribery for certain contracts from suppliers within the entire waste management industry. ESTR brought in an independent counsel to review all requested documents from the years 2010 – 2016.

The council concluded that certain disbursements weren’t, “properly supported by documentary evidence” between years 2010 – 2014. However, the counsel deemed all services included during the 2015 – 2016 period were found to be properly documented. This makes sense given the company’s drastic shift in 2015 – 2016 after hiring new management and putting in new procedures and compliance practices in place. As a result of the findings, the company took action by ending all relationships with suppliers that were found to be non-compliant and part of the investigation. Furthermore, the company terminated its relationships with most of its 2015 – 2016 suppliers that, although were properly documented, were still subjects to investigation and were, for lack of a better word, sketchy business partners.

In response to ending its relationship with such partners, the company made an accounting adjustment for 2016 resulting in a write-off of PPE items totaling $53M Real. This $53M Real related to the payments made to those partners that were not properly documented during investigation. The company believes this issue is in the past, and is focused on moving forward. I keep it as a risk because with criminal investigations, you just never know how far the string leads once you start pulling. Am I confident that management is doing everything they can to make sure something like this doesn’t happen again? Yes. Bottom-line: The investigation happened, improper documents were found during the years 2010-2014, before new management. New management came in, documents are properly accounted for.

Risk #3 – Overall Debt Burden

Debt is the company’s giant elephant in the room. I’m not usually a fan of investing in company’s with this much debt (greater than 3x leveraged), and like I mentioned earlier, if interest rates rise, it would take substantial revenue growth on the top line to not hamper the effects of the rising financing costs. I will be paying extremely close attention to their leverage ratios as the final two quarters of the year turn out. If I can see management’s dedicated effort of reducing its debt, I will be even more confident in their ability to manage it into perpetuity.

One major headwind for reducing the debt burden is the nature of the waste management industry, specifically the collections segment of their business. Waste management is a CapEx intensive industry, and ESTR’s operations are no exception. The company must spend a large amount of their cash flows on investment of its vehicles, investment in new landfills to manage hazardous chemicals. This capital intensive-ness makes ESTR not able to fully put their focus on debt reduction. The company is also focused on strategic acquisitions, which require capital. It will be very interesting to see how management allocates its capital between its three options: debt reduction, acquisitions, and capital expenditures. Right now the company uses its cash from operations to reduce debt and invest back into the business. Should the company need more money, they would likely have to do it through financing.

Risk #4 – Loss of Major Contracts

Although ESTR has a wide array of customers on both the public, private, and individual / business perspective, a bulk of their revenues come from two cities; Sao Paulo and Curitiba. Together, these two contracts make up 61.9% of their revenues from 2017. The Sao Paulo contract is currently in negotiations, and failure to renew all of the contract, or failure to lock in a good price for its contract could result in significant decreases in top line revenue growth. The company expects to be subject to competitive bidding. I think in the end ESTR will win the contract given its size, its reach, and its landfill capacity. However, there is still a chance they get under-cut. It remains a risk.

Wrapping It All Up

Estre is an extremely intriguing potential investment. The macro industry tailwinds are glaringly apparent, new management has instilled a culture of success and compliance with the highest of ethical standards, and the company is the leader in an industry that is ripe for consolidation. ESTR managed to grow revenues and EBITDA during Brazil’s economic recession while expanding it’s margins in its extremely profitable landfill business. Along with strategic acquisitions, the company has a wide moat to defend itself, from regulatory crackdowns, increased red tape, and extremely high barriers to entry on the landfill side.

Management is confident in their ability to grow revenues around 5% at an annual clip while increasing margins closer to 30% on a sustainable basis. Finally, the company was able to restructure its massive debt burden to more flexible terms, giving the company cash to work with and room to maneuver.

I am not currently long ESTR in my paper account, but will look to add a position over the next couple of weeks. It will likely start out as a smaller position (around 5%), and as my confidence builds in the business operations and in management, I would love to make it around a 10% “true” starting position. Will perhaps mix in equity purchases with warrant exposure to capture the asymmetric upside potential.

As always, shoot me an email if you have questions regarding ESTR specifically, or any of my other recent investment write-ups. Comment below if I missed something in my thesis. Please shoot holes where they can be shot.

** All information for this write-up gathered from ESTR Form 20-F, Exhibit Documents, Investor Presentations, and Waste360.com Interview.

It looks like you did a lot of work on Estre before. Why do you think the market cap has fallen to just $120M? As I understand it, the company has a moratorium on debt repayment for a couple of years, so it doesn’t seem like bankruptcy is imminent but the shares have been on a one way ride down since the 20F was filed. The shares would seem to be pricing in a total loss of the business.

LikeLike

Hey Harry,

Thanks for reading and posting your question! So after listening to managements latest call the one large reason is due to the loss of their São Paulo contract (37% impact on revenues — potentially permanent). On top of that, they have a money losing segment of their business called “Corporate” that is negatively affecting bottom line figures.

For example, their “Corporate” business segment reported a loss of $330M while the rest of their actual operations generated profits (at a growing clip).

Board of directors are being shaken up, and the CFO left for “personal reasons”.

For right now I’m content with sitting on the sidelines. I tried a starter position but quickly cut for a small loss when the selling pressure got heavy. I’m looking for positive signs from management on the next call. If I see further debt reduction, continued top-line growth, and a solid answer regarding their money-draining “Corporate” segment, I might buy back in.

LikeLike