*Idea Source: Steven Wood, Greenwood Investors

Massive selling from new ITP Regulations set forth by Apple and European departments have caused share prices of the digital performance advertising company to fall to 4x EV/EBITDA — well below industry averages. With almost all of the negative news surrounding the new privacy laws baked into the price, one can buy shares of the core operating business for extremely low multiples while getting the ancillary operations (call options) for free. CRTO sports 90%+ customer retention rates, 1% monthly churn levels and ample ROAC (return on advertising cost) to its clients — a 13x average.

Criteo touts over 19,000 customers worldwide and claims the largest Shopper database in the world, yet the company is priced as if it will never again achieve top-line revenue growth. CRTO has a path to become the go-to solution in the “Open Internet”, a third option for publishers and bidders besides the conventional FB & GOOG route. Former CEO JB Rudelle is back in the saddle, talking to investors, personally acquired stock and quickly initiated an $80M share repurchase program. Interests are aligned.

Delivering Exceptional Digital Ads

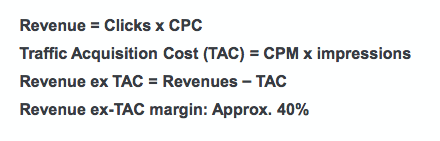

Criteo is a digital performance advertising company with a goal as simple as it is all-encompassing: Helping businesses target the right customer, with the right product, at the right time. The company does this by leveraging the largest Shopper database in the world through four main avenues of operations: Dynamic Retargeting, Sponsored Products, Customer Acquisition and Audience Match. Each line of operations works as a CPC (cost-per-click) model in which clients (hopefully) receive post-click sales. A quick primer on their model can be seen below:

Beyond The Cost-Per-Click Model

Although Criteo made famous the cost-per-click model during their IPO in 2008, management’s now turning to a full funnel framework in an effort to capture revenue across all phases of the advertising campaign. By employing a cost-per-thousand impressions (CPM) model, Criteo captures two of the three advertising objectives not named conversion: Awareness and Consideration. The objective of this full funnel model isn’t to generate sales, but rather make a warm introduction into the product, service or app. This should prove to be a nice complement to its already robust CPC conversion model.

Criteo’s Competitive Advantages

Largest Shopper Dataset in The World

All four lines of business above rely on Criteo’s massive Shopper Database: Shopper Graph. A quick fact-sheet rundown of Shopper Graph paints the picture of its immense proportions and capabilities: access to 4.5 billion products, largest consumer reach worldwide, 120+ shopping intent signals evaluating each and every shopper, 100 participating retailers and $760B in annual e-commerce transactions. Oh, and did I mention that Shopper Graph collects 600 terabytes of data every single day?

Combine the Shopper Graph dataset with CRTO’s advanced machine learning models and you have a positive feedback loop in place for a sustainable advantage. Machine learning models are only as good as the data fed through them. In other words, the more data a deep-learning model has to work with, the better predictions it will make once new data is fed through. So, one could assume that if Criteo has the largest dataset of shoppers in the world it would translate into one of the best — if not the best — machine learning model in the world as well? It would be extremely tough for a competitor to try and replicate or improve on the machine learning models CRTO has in house.

High Retention Rates, Low Churn & Happy Clients

Criteo’s solutions work, and the proof is in the stories of hundreds of happy Criteo clients. Clients on average receive close to 14x their marketing spend with Criteo, prompting nearly 80% of their client to uncap their marketing budgets. For example, Sephora (the makeup retailer) experienced 220% ROI in their first month partnering with Criteo. Fiat Turkey reduced its lead costs by 97% and sales costs by 91%. Office Depot saw an increase in ROAS (Return on Ad Spending) by 104%. The list goes on from there.

Criteo positions itself as an enterprise that benefits all stakeholders in the digital advertising chain; advertisers, consumers and publishers. The company provides advertisers with increased performance, transparency and control over their advertisements and ad-spend. Consumers benefit from increased product discovery and a consensual sharing of data to enhance the consumer’s online experience. Finally, publishers receive enhanced performance from direct access to Criteo’s Shopper Graph dataset, enabling publishers to skip the middle man (GOOG & FB) and target their customers directly.

The Only Option for the Open Internet

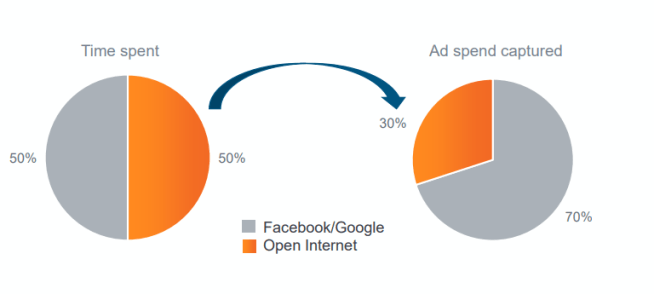

The runway is long for CRTO to turn the ship around and return to double-digit top line growth. The open internet remains tremendously under-monetized — an area the company plans to dominate. 50% of time spent on the internet goes to Facebook and Google, the other half to “open internet”. However, when looking at ad spend captured, Facebook and Google take 70% of the pie. Criteo wants to give advertisers — no matter their size — the ability to directly interact with targeted audiences and potential customers. That Criteo aims to leverage their Shopper Graph data to advertisers and publishers of all sizes shows a concentrated effort of removing the middle-man from the equation. Smaller advertisers can partner with Criteo knowing that as they grow, Criteo has the capacity and scale to grow alongside them.

Many of Criteo’s clients stress the importance of keeping direct relationships with their end users — and in the same breath — express concerns over their tremendous dependence on Facebook and Google. If Criteo can successfully label itself as the lifeline to keep and protect direct relationships with end-users, they entrench themselves into the operations of their clients — becoming an indispensable asset.

Adapting For Future Growth

Shift in Offering Model

Along with the implementation of the CPM model, the company is shifting its focus on go-to-market strategies and transitioning its sales team to a multi-solution offering. CRTO breaks down its client tiers into three categories: Large Clients, Upper Mid-Market and Lower Mid-Market.

In order to scale and drive incremental profitability, the company aims to make the Lower Mid-Market corner of their operations fully self-service. This means that clients with $5K or less in ad-spend will register, on-board, and incorporate CRTO’s features in a fully autonomous manner. By doing this, CRTO is able to reach more potential clients without increasing spending to get them. With automation, lower and mid-level clients can now on-board faster and adjust their campaign goals / settings in real-time. For its large clients (monthly ad spend between $50K – $200K), CRTO will offer its full consultative sales package. This package includes tailored service to the client’s specific needs and end-goal objectives, as well as increased insights / ad proposals from direct bidders.

Focusing on In-App Advertising

Mobile app usage is growing very quickly and CRTO is jumping in head first. According to management’s last earnings transcript, CRTO’s already experiencing demand for their in-app advertising solutions from existing clients. To meet this demand, the company acquired Manage, an in-app advertising company, for roughly 5x EBITDA. Manage is already profitable, growing top-line revenues and sports robust EBITDA margins. 5x EBITDA seems like a fair price (I don’t think they overpaid by any stretch). So what makes the app space so special?

The average lifespan value of an app customer is higher than its web browsing cousin. This makes intuitive sense as someone who downloads the app would be more inclined to purchase from the company / service. Apps also increase moats for businesses that use them. If a business can get its customer to download their app, it’s now captured incrementally more time and interest per customer at little to no cost (after app is built). Creating an advertising campaign inside apps is difficult, requiring loads of capital up-front in R&D — which CRTO has plenty and other advertising competitors can’t afford. This investment pays off, however, as in-App ads deliver (on average) higher ROAS to its clients than website spending. Since customers are spending more time inside apps, it gives CRTO a higher chance at capturing that customer. Apps are also more advertiser friendly as they don’t rely on cookies the way web browsers do.

What Caused Shares To Crater?

Three Head-less Horsemen of Digital Advertising

Criteo was hit by the “Three Horsemen” of digital advertisement nightmares in 2017 — Apple ITP Regulations, European General Data Privacy Regulation (GDPR), and losing Facebook Partner status. The largest detractor from revenue expansion was Apple’s ITP regulations, which resulted in worse than expected losses after a failed workaround attempt. The company experienced a lesser impact from GDPR than originally anticipated. Going back to Q2 transcripts, management exclaimed, “the actual impact of GDPR on our business has been quite limited and lower than we expected.” Finally, the Facebook Partner drop represents a loss of 3% ex-TAC revenues — not extraordinarily material. The biggest detriment from these regulations is that CRTO lost extensive visibility into their Safari business projections — in other words — it will be interesting to see how things shake out year-end.

Risks Still Exist

All things considered, we still don’t know for sure how bad ITP will be for CRTO in 3 – 5 years time. If we take managements word, the worst is in the rear-view mirror. However, the tide has shifted towards increased privacy and protection on the internet, not away. Not to mention, the digital advertising industry is brutally competitive. Returns can easily be cannibalized, and end-market saturation is all but assured at some point in time. That the industry will become saturated and returns cannibalized suggest that over time businesses will spend less on advertising, citing lower returns on ad spending.

Criteo Doesn’t Need Ridiculous Growth To Win

Shares of CRTO have fallen nearly 60% from the highs. The company’s EV/EBITDA multiple went from 17.5x to 4.5x and you can now purchase shares for less than 4x 2020 EBITDA. Criteo has $7 in net cash per share and no debt. If we assume zero top-line growth from current figures and slap a modest 10x multiple on EBITDA we arrive at a fair value range of close to $34 (40% upside). Taking the DCF approach we arrive at an EV of $1.08B, add in net debt and divide by shares outstanding gets us ~$21 (12% downside). Now, if we assume a meager 5% top-line growth trajectory and a resulting multiple expansion to 12x (still below industry average), we end up with fair value close to $41 (71% upside), and an intrinsic cash flow fair range of ~$24.

If we assume 10% top-line growth (bear in mind CRTO was growing around 30% top-line a year ago) and an EV/EBITDA multiple of 15x (closer to its pre-ITP days), we arrive at a relative fair value of around $68 (181% upside). Using a DCF model gives us fair value between $28 – $30.

So, what if revenues declined 10% each year for the next five years? If we assume a lower-than-average EBITDA multiple to that scenario we still get a fair value knocking on ~$20/share. So here you have a business trading at all time low valuations, net cash on the balance sheet, an aligned management team and a path to a double or triple without needing to return to 30%+ top-line growth.

Downside protection comes in the form of an excellent balance sheet, ample insider buying at these low levels and the fact that CRTO looks and smells like a great acquisition target. I sleep well at night knowing reinstated CEO Rudelle purchased over $500K in shares upon his arrival and quickly initiated an $80M stock buyback program. I’m not in the business of predicting stock bottoms, but management clearly is excited about the current risk/reward given the share price, and I am too.

Tough week. Any thoughts post the Google announcement?

LikeLike

Hey KRS —

Thanks for taking the time to read the write-up. A tough week indeed! We’re on the sidelines right now waiting to see how things unfold. We initially established a “tracking” position in the business because of this very risk. We got out of the investment once the news broke — reason being we did not know what the ramifications of this news would do for the future growth prospects of the company.

In situations like this I find it valuable to be able to get out for a small loss, re-evaluate the long-term thesis and then decide a good point to buy back in. Too many unknowns right now with privacy laws of Google — and you’re seeing a heavier push from Apple’s Safari for increased privacy and less website tracking (this could be recency bias as I’ve noticed an uptick in those types of commercials).

Sitting and waiting for the time being.

LikeLike