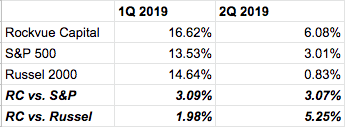

The Rockvue Capital paper fund returned 6.08% during the 2Q 2019, outpacing the S&P 500 by over 300bps. Year to date, the Fund has returned 22.70% compared to the S&P 500 return of 16.54%. I stress that any short-term performance be taken with a grain of salt, as the Fund should stand on its five-year track record. We take concentrated bets in a select number of businesses. As a result, our performance may deviate significantly compared to the broader market; sometimes to our benefit, sometimes to our detriment.

The Fund holds a collection of great businesses that generate cash, are led by incentivized management and have long run-ways for growth and multiple expansion. During the second quarter, the market rewarded a handful of our holdings through share price appreciation. At the same time, a few of the Fund’s highest conviction ideas remain stuck in the voting machine phase of Mr. Market’s lifecycle.

Over the course of this letter we’ll dive into the following:

- Our top holdings

- Provide commentary on select investments (and a new short)

- The allure of higher prices

- The value of not being the smartest guy in the room

Although we released the letter weeks after quarter-end, performance stats are from 04/01/2019 – 06/30/2019.

Top Holdings

The Fund’s top five holdings are (in order): Discovery Communications (DISCA), Construction Partners (ROAD), Garrett Motion (GTX), frontdoor, Inc. (FTDR) and GrafTech (EAF).

DISCA, FTDR and ROAD drove a significant part of the Fund’s returns for the quarter. For reference, ROAD returned 20%, FTDR 27% and DISCA 10.6%. When three of your top five holdings generate double-digit returns, the Fund will do well. Yet, it’s at this point I redirect your attention to the last sentence in the opening paragraph of the letter.

During the quarter we preyed on Mr. Market’s erratic mood swings and added to each of the top five positions. At one point, DISCA made up close to 20% of the Fund’s assets — the highest any position has reached in Fund’s history. ROAD leap-frogged GTX and FTDR due to increased purchasing and share price appreciation. As it stands, we’re not looking to add to our 12% position unless shares drop from current valuations.

Share Price Not Reflecting Intrinsic Value

GrafTech (EAF) and Target Hospitality (TH) continue to drag on the Fund’s performance, with shares falling 13% and 10%. While frustrating, we remain encouraged as both businesses are operating well. GrafTech is on pace to generate around $800M in FCF in 2019, implying a FCF yield of 24%. Paying 4x earnings for a 24% FCF yielding business is a bet the Fund will take any day.

Target Hospitality’s shares followed similar paths with that of most SPACs — straight downwards. While share prices fell, the earnings and news from the company were positive. Management revised full-year 2019 guidance upwards during their latest earnings report. CEO Brad Archer bought $300K worth of stock. Capping it off, TH broke ground on new 200-bed and 400-bed projects within the Permian/Delaware Basins.

We continue to look for spots to add to TH. Looking back, we made the mistake of taking too large of a position early on in our investment horizon. This mistake has restricted us from averaging down in the position as share prices fell. We’ve added this mistake into our “Try Not To Make Again” pile.

We’re hopeful Mr. Market will realize the true intrinsic value of both assets. Unfortunately, we don’t know when that will be.

New Short: Under Armour, Inc. (UAA)

To be transparent, I’m not great at shorting. The Fund hasn’t lost a lot shorting, but it hasn’t made significant sums either. I prefer to spend 99% of my time searching for businesses we can invest in for long periods of time — letting the nature of compounding work in our favor. But sometimes I come across a business whose valuation doesn’t make sense. One such business is Under Armour (UAA).

The short thesis for UAA is simple. Here’s a business that’s reported -3% sales growth in their “best” market (the US) for the last three consecutive quarters but trades at 60x 2019 earnings and 21x 2019 EBITDA. Bolstered by robust 12% international growth, total sales growth is a meager 1% through 2H 2019.

I don’t see a world in which it makes sense to pay 60x earnings for sub 5% top-line growth, let alone 1%. In fact, the company’s failed to break 5% revenue growth over the last two years — yet still commands a 60x multiple. Have I mentioned the company is in the retail space?

When comparing Under Armour to a competitor, such as Lululemon (LULU), the overvaluation becomes even clearer. LULU’s grown top-line revenues by 13% and 24% over the last two years respectively. Shockingly, LULU sports a lower multiple than its struggling peer. You can buy LULU shares for less than 40x next years earnings. Not only does LULU make better-feeling performance wear (anecdotal), but you can buy the business at a 33% cheaper valuation than UAA.

Given the unfavorable dynamics of shorting (potential for unlimited loss, etc.), we’re monitoring our position with stop-losses. The stop-loss caps our loss to the upside while enabling us to move towards breakeven as share prices decline. Shares are down roughly 10% since initiating our position.

The Allure of High Prices: When Price Equals Quality

Traditional economic theory claims that humans make rational choices at the margins. Yet as author Dan Ariely reveals in his book, Predictably Irrational, this couldn’t be farther from the truth. Ariely offers countless examples throughout the 300+ pages. For our purposes we’ll focus on one behavior: the power of price.

We tend to associate higher price with higher quality, as Ariely explains,

“On the basis of price alone, it is easy to imagine that a $4,000 couch will be more comfortable than a $400 couch; that a pair of designer jeans will be better stitched and more comfortable than a pair from Wal-Mart; […] that the roast duck at the Imperial Dynasty (for $19.95) is substantially better than the roast duck at Wong’s Noodle Shop (for $10.95).”

Looking at this phenomenon from a pharmaceutical perspective we gain insight into how we think about prices in the stock market. In an experiment to determine if price impacts perceived pain relief from a pill, Ariely discounted a placebo pain-relief pill from $2.50 to $0.10.

After discounting the price of the drug, the results were startling. Ariely reveals (emphasis mine),

“At $2.50 almost all our participants experienced pain relief from the pill. But when the price was dropped to 10 cents, only half of them did.”

In other words, price can change your experience.

This relates to investing in two key ways:

- Companies whose stocks get bid higher and higher can feel like safer investments. After all, they’re a high share price for a reason, right?

- Companies whose stocks get slammed lower and lower can feel like riskier investments. After all, they’re trading at such low valuations for a reason, right?

This is, of course, an overgeneralization, but the point remains: price changes our experience about a company. That’s not always a good thing! Seeing a stock price trade lower makes us wonder if our thesis was actually correct. Then, if a stock rises after we buy, we pat ourselves on the back because of course we made the right decision and our analysis was spot on — even if we were actually dead wrong in our thesis.

Not Being The Smartest Guy in the Room

In June I had the incredible opportunity to attend ValueX Vail 2019. The conference is dedicated to diehard, hardcore value investors and run by Vitaliy Katsenelson. During the four day trip I connected with 40 investors, most of whom ran their own funds, family offices or partnerships. There were over 20 stock pitches and countless discussions on investment philosophy, education, science and valuation. Yours truly pitched Target Hospitality (TH) on Day 1. You can download the slide deck here.

I wasn’t the smartest person in the room, and I loved it. As this was my first time attending the conference, my goal was to be a sponge, absorbing all that I could from each person in attendance. Trying to ask good, thoughtful questions was a goal, but my priority was to listen. Listen and absorb. If you have the chance to not be the smartest person in the room, take it. I can say with 100% certainty that I left that conference smarter than when I arrived.

The more knowledge I gain, the more I realize how little I know. Although it sounds depressing, I view the claim with extreme optimism. There will always be ways to get better. New models through which to view the world. Opportunities to go to bed smarter than when I woke up.

Closing Thoughts

The hurdle rate for new investments in the Fund is at its highest point since inception. While I spent most of the quarter searching for new investments, the majority of our purchasing took place in existing holdings. Stocks are ownership shares in physical businesses, not blips on a computer screen. We own good businesses, bought at cheap prices, with long runways for margin and multiple expansion. When fake-meat companies trade over 100x sales, trade wars escalate within 280 characters and performance time horizons shrink to months (not years), our competitive advantages as a fund hold true. We continue to focus on buying great businesses at ridiculously cheap prices. We will not chase the newest shiny object.

Readership has increased since last quarter, so to new readers, welcome. I look forward to reporting to you in October.

Always enjoy reading these

LikeLike

Thank you! Means a lot!

LikeLike