Jemtec, Inc. (JTC) is a nano-cap company that trades on the Toronto Venture Exchange (TSXV). At current prices, you can buy the business for around $4.2M, or a little over $2M net of cash. It’s very small.

All figures will be in CAD.

Background & Thesis

The company is Canada’s leader in electronic tracking technology. JTC specializes in public and private offender monitoring/tracking. They help governments track past offenders.

Jemtec’s helped their clients track over 50,000 individuals since 1987. The company’s a leader in a niche business with high switching costs. The business is somewhat recession resistant. Prisons and correctional offices need to track criminals that are out in society. No matter where we are in the business cycle.

JTC’s solutions enable governments and organizations to focus on other areas besides monitoring. Their solution is mission-critical, and if I had to guess, this business will be around for the next 20+ years.

Here’s the interesting part. You can buy this business for around 8x earnings and 3x EBITDA. The company sports a robust balance sheet with half its market cap in cash, zero debt and around $0.80/share in NCAV. The CEO owns 20% of the business and is a 28 year veteran. Interests are aligned.

JTC wasn’t a high-growth business pre-2016. They barely grew top-line from 2010-2017. Yet between 2017 – 2018, the company’s grown revenues 34% and 52%.

It looks like the company’s gained momentum in revenue growth. 2019 figures reveal 25% top-line growth. The recent surge propelled the company to two-year positive EPS of $0.01/share and $0.09/share.

How Jemtec Makes Money

The company’s business model is “project driven”. They sign long-term contracts with correction facilities, governments, courts, prisons and private individuals. According to their latest MD&A, most of the projects renew after the initial project timeline.

There’s three recent examples of JTC’s sticky-ness as a business. In 2015, Jemtec signed a three-year deal with Public Works and Government Services Canada (PWGSC). The contract provides Electronic Monitoring (EM) solutions. At the end of the contract, PWGSC picked up both extension options.

Then in 2016, JTC signed a three-year deal with Nova Scotia Justice Department. The contract offered JTC’s offender monitoring services. After the three year term, the Justice Department exercised their first two-year extension.

In 2017, JTC entered a three-year term with the Province of Saskatchewan. The original term expires March 2020 — but the Province has two, one-year extensions. Later that year, the company signed a four-year contract with Ontario Minister of Community Safety and Correctional Services (MCSCS). The deal provides electronic monitoring equipment, technology, software and technical support to MCSCS. The services fall in line with MCSCS’ Supervision Program. Like previous agreements, the MCSCS contract allows for two, one-year extensions.

Three Operating Segments

The company recognizes revenue through three segments:

- Leasing, monitoring and activation

- Bail

- Interest Income

The leading driver of revenue is, of course, their leasing, monitoring and activation services (>90%). The company breaks down their leasing, monitoring and activation revenues into two broad categories:

- Government agencies

- Private monitoring

Let’s flesh these out.

Government Agencies

Government agencies includes immigration, police and correctional services. These are sticky end customers. Once a system integrates with a government agency, it’s hard to remove that system. Even if there’s a better one out there. We’re talking both hardware and software. That’s expensive to replace.

Let’s take correctional services as an example. These services need a system to track criminals as they enter parole or finish their sentence. It’s a mandate that protects the public and provides a “CYA” filter for correctional services.

JTC’s services also double as a compliance tool. The company’s services track house arrest, home curfew, alcohol abstinence and movement restrictions. This frees up the correctional facility to focus on what matters. Integrating these men and women back into society. At the end of the day it’s about the public’s safety. Will government agencies skimp on this investment? Probably not.

Now, let’s take a look at the immigration side. The Canadian Border Security Agency (CBSA) handles varying types of immigration judgements. For instance, some immigration cases are for hostile individuals. These cases need in-house detention. Yet, the majority of immigration cases involve some release of custody. In these instances, JTC enables the CBSA to track these immigrants under heavy restrictions. Restrictions such as house arrest and geographic dependency.

Finally we have the police division. Law enforcement spends a lot of money dealing with high-risk, repeat offenders. Such offenders often require 24 hour surveillance. This costs the department time, money and resources (able police bodies). Such tracking criteria includes:

- Home curfews

- Restricted Areas (such as playgrounds, schools, parks and airports)

In other words, these are vital services JTC provides to many levels of government.

But they also service private individuals.

Private Monitoring

The company’s offered private monitoring services since 2004. These private monitoring solutions allow defense lawyers to present a compliance review for the judge and jury. These reviews say that “John Doe” went home at curfew and didn’t enter playground zones. It shows they played by the rules. This helps when it comes time to decide on parole or release dates.

(Relative) Fixed Costs, Upside Operating Leverage

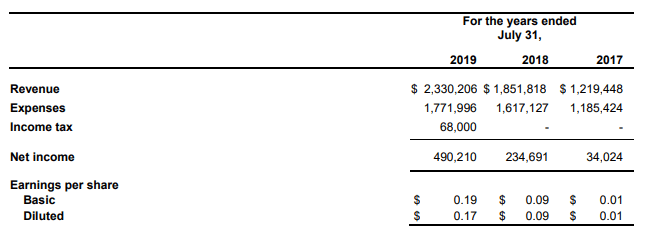

Check out the company’s consolidated results over the last three years:

The company’s expanded gross margins from 2.70% in 2017 to 24% in 2019. That’s a 787% increase. They’ve also grown EPS 19x during that time. JTC’s growing revenues at 20%+ while increasing expenses by 10%. This is a recipe for success. Their model scales as they sign new contracts and enter longer extensions.

If you exclude the income tax, the company’s grown EBIT by 138% from 2018 ($550K in 2019).

So why has the company grown so fast over the last two years? A slight change in their business model. Normally, JTC signs lease agreements, which provides equipment, servicing, consulting and tracking. All in one. Then the company introduced a “rental” revenue segment. In this case, a local government or correctional facility rents the monitoring equipment on a daily basis.

According to management’s notes, they offered the rental segment “to allow Provincial and Federal customers the risk reduction and flexibility to start programs that in some cases would not have happened without the rental component.”

The rental offering allows customers to dip their toes into JTC’s broader offerings — without most of the longer-term commitment. This is a great model. The company already has the equipment. Now, they can monetize that equipment that they otherwise wouldn’t use. I could be wrong in this framework — but the rental offering functions as an accretive customer acquisition cost. In other words, JTC’s making money on new customers with the call-like option of future contractual (leasing) agreements.

A Flawless Balance Sheet With Loads of Cash

JTC has a cash-heavy, fortress-like balance sheet. The company has $2.5M in current assets and $406K in total liabilities. That’s a net current asset value of $2.09M. Even better, the majority of the company’s current assets are in cash or cash equivalents. So in a sense you’re getting a net cash value of $2.09M.

The company has no long-term liabilities. And they’ve reduced current liabilities by $280K YoY while increasing assets $400K.

This is one of the better balance sheets I’ve seen from such a small company.

But that’s not all.

Check out this paragraph from management’s annual report notes (emphasis mine):

“All of the Company’s financial liabilities are classified as current and are anticipated to mature within the next fiscal period. The Company intends to settle these with funds from its working capital position.”

This means that by next fiscal year, the company will have zero liabilities on the balance sheet. If that’s the case, the only real liability the company has is their lease obligation of $1,807/month.

On top of that, there’s also the possibility the company understates their book value. For example, they value their monitoring equipment at $603K. At the same time, they account for $520.4K in accumulated depreciation.

This leaves us with a mere $83K book value for the monitoring equipment. That could be correct given the nature of technological improvement. But what if the equipment is worth more than what they’re stating? That raises the company’s book/asset value by roughly $500K or so.

Valuation

We know the company will have zero total liabilities next fiscal year. We also know the company’s expanded margins, grown revenues and generated nearly $500K in after-tax operating earnings. Let’s take a look a few scenarios: liquidation value, no-growth value, optimistic growth value.

Liquidation Value

The company’s got $2.58M in total assets and $406K in total liabilities. That gives us a net asset value of around $2.1M. Dividing that by 2.83M shares outstanding gives us $0.75/share in value. But, if we throw in a higher valuation for the equipment (besides the $83K on the current balance sheet), we’d get closer to $0.85 – $1.00/share.

The stock trades at $1.55 as of writing (12/12).

No-Growth Valuation

If the company doesn’t grow at all over the next five years, we’re left with around $11.65M in cumulative revenue. $3.56M in free cash flow (after-tax earnings + D&A – NWC).

That gives us around $7.6M enterprise value. Adding back the net cash (around $2M) and we get market cap of $9.6M. This gives us around $3.40/share in intrinsic value (over 120% upside).

All this assumes the company’s able to maintain margins and doesn’t dilute shareholders.

Cautious Optimism

JTC’s averaged 29.76% revenue growth since 2015. For the sake of modeling, we’re not assuming that high of growth. Over time, growth should revert back to a lower mean (whatever that is).

Let’s assume 10% revenue growth over the next five years. In this world, we’re left with $3.75M in 2023 revenues, $780K in after-tax earnings and $960K in FCF (2x EV/FCF). It also gives us a cumulative FCF of $4.58M, and $11.71M enterprise value. If we add back the net cash, we’re left with $13M market cap. Divide that by 2.83M shares and that’s almost $5/share in intrinsic value.

Risks

There’s a few main concerns with Jemtec:

- Increased Share dilution

- Government contracts = lowest-cost bidder war

- Incomplete data on efficacy

Increased Share Dilution

The company’s increased diluted shares by 200K from 2018. While this isn’t alarming on its own, a continuing trend of share issuance is a concern. But I don’t think this will happen. CEO Eric Caton owns 20% of the shares outstanding. Any further dilution reduces his ownership.

Nature of Gov’t Contracts

In most instances, competing for government contracts results in a lowest-cost bidder. This type of auction drives prices (and profits) lower for everyone involved. The key, of course, is to lock in those three-to-five year contracts with 1-2 year extension options.

This makes JTC’s revenues more lumpy on a quarterly basis (which management acknowledges), but over time should smooth upwards.

Incomplete Data on Efficacy

According to Canada’s public safety website, the rate of recidivism wasn’t noticeable between correctional facilities using EM (electronic monitoring) and those opting for traditional probation.

Yet it’s important to distinguish the cost-effectiveness on a pure dollar-basis vs. the safety of the community. Communities feel safer knowing there’s electronic monitoring watching high-risk criminals. Even if the pure dollar cost-savings isn’t a significant statistic.

Conclusion

I’ve got a small, starter position now. I would love for the stock to drop to ~$1/share. At that price, you’re buying a balance sheet with $2M in cash and no liabilities. You’re also getting a profitable, growing operating business for free. That’s not a bad deal. As long as management executes, grows revenues and maintains margins, investors should be handsomely rewarded over the next five years.

Just had a quick look at this. CEO compensation was $280k-$300k for 2013-2018 (base salary $240k) each(!) year while the revenue of Jemtec was less than a million until 2017.

That’s a clear pass for me.

LikeLike

what are the odds this company gets bought out? By my estimation the CEO is at minimum 65 years old. The only way he unloads his shares is in a buyout. Do you have any awareness of competitors or larger similar companies that could swallow them up?

LikeLike

Hey Philip —

Thanks for reaching out! I’ve tried to get a hold of management to discuss this question. After doing some research, the only other comps around them specialize in actual product manufacturing (such as ankle tracker bracelets, etc.).

In other words, I need to do more work and will keep you updated.

Feel free to email me themarketplunger@gmail.com for further questions.

Thanks!

LikeLike

What are your thoughts on the one time special dividend? https://www.newswire.ca/news-releases/jemtec-declares-a-one-time-special-dividend-869357444.html

LikeLike

As a general rule, I’d prefer share buybacks as they’re more tax-efficient for shareholders. But I cannot complain about a special, one-time 17% dividend on my investment.

Management’s reasonings were very positive too … They basically admit that their business is capital-light, generates a ton of free cash flow, and that they’ll have no issue re-cooping this one-time cash outlay.

LikeLiked by 1 person

Thanks for the blog and this specific post. I had never heard of this company prior to your blog post.

LikeLike

Thanks Philip! Means a lot!

LikeLike

Q2 earnings out – https://sedar.com/GetFile.do?lang=EN&docClass=8&issuerNo=00007599&issuerType=03&projectNo=03035107&docId=4690547

Pretty sure COVID-19 won’t be hurting their business.They are still sitting on a boatload of cash and have signed a new agreement with Correctional Services Canada.

LikeLike