If you’ve stuck around for Part 2 of my Russian Bull Thesis, congrats! If you haven’t read Part 1, check it out here. I won’t bore you with Part 1 review, so I will give a brief overview. Part 1 dealt with the Russian economy as a whole, which returned a bullish hypothesis after my research. Secondly, it investigated different ways to play this Russian bull thesis. Part 2 is going to deal with the third option in which to invest in Russia: Direct investment in Russian Companies.

Asymmetric Trade Potential

Asymmetric trading is what I base my portfolio and investments off of. I want to find the opportunities where I risk the least to gain the most. Ed Seykota is a legendary technical investor, if not the greatest in terms of reading price action. If you haven’t read some of Seykota’s stuff on his site TradingTribe.com, you’re missing out on amazing nuggets of information. In one article, Seykota talks about risk reward scenarios. Ed likes to stay at least around 3:1 risk reward, meaning he likes to risk 1% of his money to gain 3% on a trade. Making three times your investment is good enough for Seykota, so its good enough for me.

Now, when searching for the best way to create asymmetry in the Russian investment, its important to look at liquidity, risk, and potential gain. The first way I looked at investing in Russia is to buy the Ruble. This is a great way to play the rise in the Russian Economy, but in terms of exponential growth over a shorter period of time, this isn’t the investment. The Ruble is a longer term play for my portfolio, and because of that my stops are set pretty far back from where the current price is. This way, if my stop gets hit, it is a signal of a reversal on a longer term trend.

Secondly I bought the RSX Russian ETF for my paper portfolio. Compared to the Russian Ruble investment, investing in RSX would generate faster returns, however, I don’t think it is the best way to capture the long side of the Russian Bull market.

Two Companies To Target

1. PJSC Gazprom (OGZPY)

Gazprom PJSC is engaged in the exploration, production, transportation, and sale of gas in the Russian Federation and other countries. Gazprom was founded in 1993 and over the course of the last year has declined roughly 4%, but even more interesting is the 5 year track record. Over the last five years, Gazprom has declined 58%, something I love to see in turnaround/contrarian investment opportunities. Before we get into the fundamentals and technicals of the company itself, its important to take a step back and look at the global macro perspective.

The financial numbers from Gazprom are the financial numbers with the sanctions kicked in. What does this mean? Simply put, we can safely postulate that reduced sanctions on Russia would only increase the potential for profit within Russian corporations. Now, with that being said, what is the current industry being hit the hardest? Oil & Gas and Energy.

Gazprom Financial Information

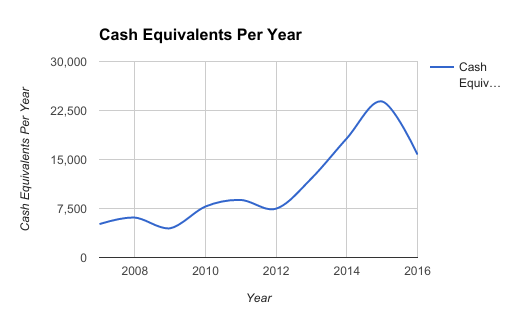

When looking at potential investments, I love to check the cash and asset positions first. Why is that? To me, cash is king in business. Cash is the most liquid form of an asset in any company or individual. I have found that companies with relatively high cash positions perform better in times of distress. Companies with heavy cash positions are better suited to ride out rough times. Since 2007, Gazprom’s cash position has increased tremendously.

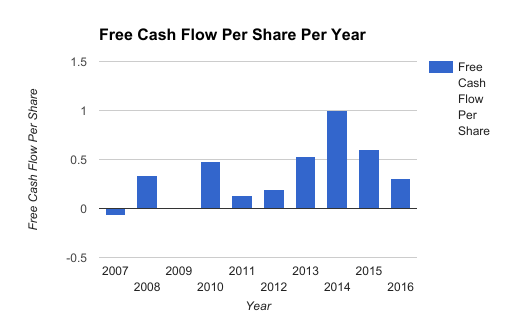

Where this heavy cash position comes from is through cashflow from operations and free cash flow. Free cash flow is the life blood of a company, and increasing cash flow signifies increased probabilities of success in business. Taking a look at Gazprom’s free cash flow per year, we see a nice upward trend, however not without hiccups. Since 2014, Gazprom has seen its free cash flow per share decline, mostly due to increased sanctions on Russia.

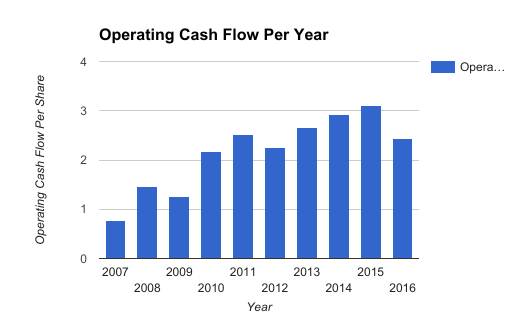

Following free cash flow, we have cash flow from operations. One interesting thing to note from this chart is the steady, consistent growth seen over the last 9 years.

Next, lets take a look at some fundamentals per share to get a better look at the valuation that could be exposed.

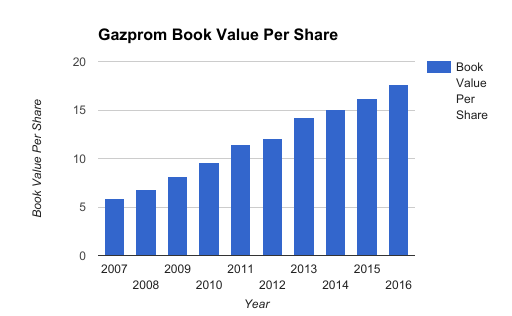

Gazprom has experienced tremendous growth in their book value, which reflects the growth in the book value per share. What’s interesting to note is the steady consistency, with no drops in book value per share over the last 9 years.

Following Book Value Per Share, we have Price to Tangible Book Value. Once again, the important trend to realize is the decreasing price to TBV.

Judging by book value, Gazprom is trading at a 73% discount. According to discounted cash flow models, Gazprom is trading at a 74% discount to fair value. Even taking a look at the Graham Number (a fair value price that is extremely conservative) Gazprom is trading at a 80% discount to Graham Number. Now, there are some things that could be potential red flags in the business, for instance, the debt Gazprom is taking on. The chart below shows the total debt per share since 2007. Time can only tell if the decrease in debt from 2015 to 2016 will signify a trend lower in debt.

In terms of valuation, Gazprom’s EV – EBITDA ratio is at its lowest level since 2013.

Technical Analysis & Price Action

Taking a look at the weekly price chart, you can see a bit of consolidation towards the beginning of April and into end of April. What is interesting to note is the 50 MA crossover that you see over the course of the last two weeks. After selling off last week, I am looking to see if it holds that 50 MA. If it can hold that average, and use the 50 MA as a support line, it would make me a lot more comfortable initiating a long position.

I’m not in any hurry. I am waiting for the price action to reveal the bullish narrative to me that I am hypothesizing. One thing that I’m learning is that it doesn’t matter AT ALL what I think about a certain stock, commodity, future, or index … What matters is the price action. My opinions don’t actually possess any merit. They are merely the lens in which I view an investment instrument. By not caring whether I am right or wrong, it frees me up to look at the second level of trading, to think about how other investors are thinking about a stock or market.

Nevertheless, if the price action does work in my favor, I would look to enter around the $4.80 – $4.85 level. With that in mind, I would place my stops around the $3.95 – $4.00 level, as always, risking at most 1% of my portfolio on this trade.

Moving on to the next company!

2. AO Mosenergo

AOMOY and its subsidiaries is engaged in generation of heat and electric power and heat distribution services in the Moscow City and Moscow region. The Company’s power and heat generation base includes 15 power plants with operational capacity of 12,737 megawatt and 42,264 gigacalories/hour of electricity and heat capacity.

AOMOY (unlike Gazprom) saw tremendous growth over the last year, shooting up 143%. But, over the last five years has suffered similar fates as most Russian companies, falling 14%. There are quite a few reasons why AOMOY peaked my interest, but lets begin with their business. AOMOY provides heat and electric power, and they distribute those heating and powering services to Moscow City and the Moscow Region. I went to the company’s website and lo and behold the entire website was in Russian. Even though I am teaching myself Russian, I could not make-out any of the website. Thanks to the magical powers of Google, I automatically translated the website so I could read it in its English translation. Here’s a snippet of what the company says about itself.

PJSC “Mosenergo” – the largest territorial generating company in Russia and one of the largest heat producer in the world. As part of the company has 15 power plants with installed electrical capacity of 13 thousand. MW. Also in the “Mosenergo” functioning regional and quarterly thermal stations, regional stations teploelektrosnabzheniya. Installed heat capacity “Mosenergo” – 43 Gcal / h.. Power plants of PJSC “Mosenergo” delivers more than 60% of the electrical energy consumed in the Moscow region. The company provides more than 80% of Moscow needs (excluding annexed territories) in the thermal energy.

Immediately what stood out to me was the first and last parts of the paragraph, which are worth repeating here: “The largest territorial generating company in Russia and one of the largest heat producers in the world” and then, “The company provides more than 80% of Moscow’s needs in thermal energy” (www.mosenergo.ru/). But what really interests me isn’t necessarily the energy and heat that they generate and distribute that energy, its their other businesses within the company, specifically their businesses in agricultural products and feed water sales. Water and agriculture have been an interest of mine in terms of an investment for around 2 – 3 years, and to be honest, that is for another post. Long story short, I believe in the power of supply and demand, and with more and more people being born, the demand for farm land and water will skyrocket.

Right off the bat this looks interestingly similar to Warren Buffett’s strategy of investing in large, durable businesses with a competitive advantage. Providing more than 80% of Moscow’s energy needs is definitely a durable competitive advantage. Now, let’s dive into these balance sheets and see if we can decode what it says (both literally and figuratively).

To be honest, this was one of the hardest companies to research, mainly due to the language difference, but also because the physical PDF copy of AOMOY’s annual report is only in Russian. However, I was able to download an interactive version of their financial statement which provided me with financial data going back over the last three years, and with help from CapitalCube.com was able to gather enough evidence to come up with definable hypotheses.

Financial Findings

Starting with Revenues, AOMOY increased their revenues from 14 – 15 by 3.6%. Gross profit was increased by 22%, and net profit shot up from 1,405 RUR mln in 2014 to 6,411 RUR mln in 2015. Noncurrent Assets have increased since 2013 from 189,072 to 205,662 in 2015, and an increase of 3.1% YoY. Current assets have also experienced a nice up

trend, with current assets totaling 50,860 in 2013, to 69,823 in 2015. Long – term Liabilities have increased a good amount from 29,755 in 2013 to 60,328 in 2015. Current assets still outweigh long-term liabilities, which is always a good sign. Finally, short-term liabilities decreased 6.9% YoY from 19,120 to 17,797 in 2014 and 2015 respectively. Breaking it down into Revenue from Heat Energy, AOMOY increased sales from heat energy by 5.6%.

The fuel supply is something to be scrutinized a bit more as well as I dug into the annual report. Natural gas accounted for 97.26% of the overall breakdown of the company’s fuel balance. This means that the profits are very closely tied to whatever the price of Natural Gas is. I enjoy these types of trades because if I can spot a trend in Natural gas on the long side, buying AOMOY would in effect be a long call option on Natural gas without the theta (which is very similar to my TGD play on Gold, which I have a writeup on TradingView.com here).

Going ba

ck to the Balance Sheet Analysis, I found that their current asset structure is heavily weighted in accounts receivables, which means they have a lot of business going on. Accounts Receivables accounts for 74% of assets, reserves 12%, cash 7%, and cash and short – term investments at 7%.

Looking at the employment of the company I saw that staff turnover was only 5.20%, which is very low for a company and it makes me feel good about the management of the company.

I wanted to find as much as I could about the water and agriculture business, but I wasn’t able to find much. One thing I found from the European Bank for Reconstruction and Development was the project loan description on their water project. From the website it reads:

The company has developed a Strategic Environmental Programme to the year 2010 that identifies pollution control measures to improve the company’s environmental performance. The Programme is based on emission control and water and waste-water treatment projects which are consistent with best practice technologies implemented in western Europe.

That has me interested, and I think the future of water consumption will continue to be a highly discussed topic, and it will lead to the demand of water skyrocketing.

Valuation Ratios

AOMOY is trading at roughly 7 times earnings, 0.38 times book value, and 0.49 times sales, and 4 times free cash flow. It’s margins and returns on investment, equity, etc. all are at least 4% or higher. It is trading at a 70% discount to its book value, and 50% discount to its sales. AOMOY trading at a 66% discount to the Graham Number. Looking at its Discounted Cash Flow Model, AOMOY has a fair value of $3.19, presenting a discount of nearly 50%. Finally, its Earnings Yield is 20.45%, making it better than 96% of the companies in the Global Utilities Sector.

Technical Analysis & Price Action

Now I know what you’re probably thinking … ‘That looks extremely illiquid.’ You’re correct. It is very illiquid, which is why I like it so much. The more illiquid the stock, the more protected it is from a larger market downturn. Also, the more illiquid it is now, the more room for becoming liquid in the future it has.

In terms of an entry price, I would enter at this price, and put a stop-loss at the $0.70 mark. Once again, risking 1% of my capital on this trade. Side – note: Illiquid stocks become less of an annoyance if you have solid risk management in place. If the company hits your stop, you’re out. If it doesn’t, you keep riding the trend, not necessarily worrying about when to liquidate.

Final Comments

As always, please shoot holes into these hypotheses on these two companies. Even better, if you find a company you think would be a better investment, don’t hesitate to run it by me. I want to be challenged on my theses because through challenging predetermination does one gain a better understanding of the market as a whole. I am a strong believer in the Russian bull market comeback. Does it help to know that legendary trader Jim Rogers also thinks the same? Of course. But I don’t want to copy anyone 100%. The numbers just make sense. I’m following the numbers, I’m following the facts. No emotional ties, just statistically backed hypotheses.

Both of these companies interest me tremendously, but I’m not emotionally tied to either of them, nor am I emotionally tied to being right. I don’t care if I spend close to 3,000 words writing out a hypothesis on a certain stock or market. If tomorrow news comes out that proves my theories wrong, I respond, adapt, and adjust accordingly.

Learning to become a global macro investor is a fun one, but also a lonely one at times. Sometimes I feel like the only person looking in areas like Russian Utilities. However, in order to get results that are different from the herd, you have to move, look, and act differently than the herd. In the prime days of index funds 2017, it is much easier for my investment ideas to feel contrarian and ‘out there’. Fortunately I believe I have the personality to not only face that, but to embrace it.