Valuation is a vital step in the process of investment analysis. Without proper valuation work, an investor cannot fully gauge the validity of their ideas. There are various tools investors have at their disposal in order to value companies, such as multiple valuation (EV/EBITDA), net asset value, sum-of-the-parts (SOTP), discounted cash flow (DCF), book value, etc. These tools should be just that, tools. What makes a woodworker excellent isn’t the specific tool that she chooses (although it helps!), but rather the ability to take an idea, conceptualize it, put thoughts into actionable judgements and execute on said idea.

Although I spend most of my time researching companies and trying to value businesses, a recent exposure of slip-shod valuation work (discussed later) via Twitter motivated me to write an op-ed on the dangers of poor modeling — and to offer solutions on how to remedy these potentially crucial mistakes. The crux of my argument is as follows: Failure to properly underwrite an investment idea at conception leads to audacious levels of modeling abuse at the end.

Keubiko’s Unmasking

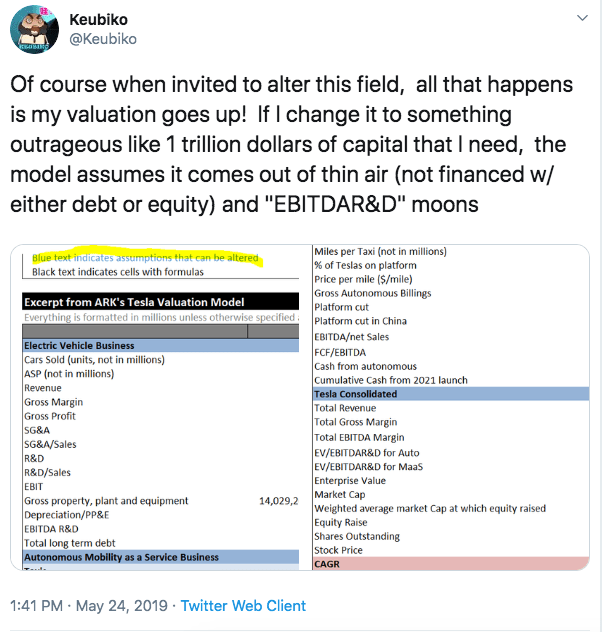

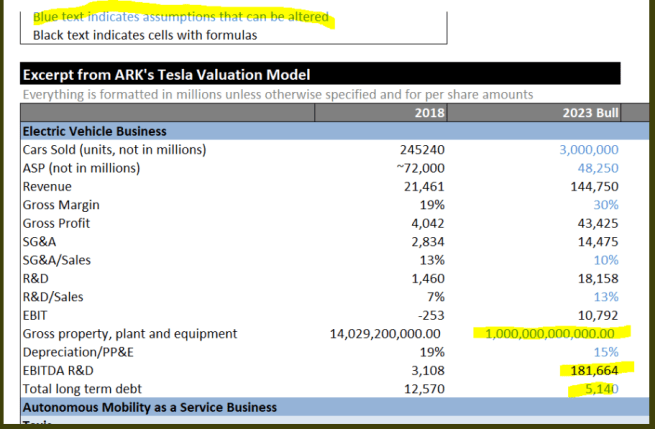

Two days ago, Twitter user @Keubiko exposed a financial model released by Tasha Keeney of Ark Invest (see below) on their valuation of Tesla (TSLA). Keubiko discovered (upon less than a minute going through the model) that the bull case hid zeros on PP&E to make it look like $19B, but was actually coded as $19,000! If only Elon and his accountants could do that in real life!

The formatting blunder wasn’t the end of the model’s shenanigans — the more Keubiko dug, the more dirt he found. Further investigation uncovered that the model was mixing Gross and Net PPE when analyzing comparable companies. For example, the model used Ford’s (F) net PPE of $35B instead of the actual $56B figure. Given the auto manufacturing business is a capital intensive enterprise — these figures make a big difference when extrapolating an equity value per share number. This is where the real fun begins! Given this PPE error, one could quickly adjust the figure within the model to come out with a more realistic picture of the balance sheet. Pay attention to the magic that happens when Keubiko attempted that change on ARK’s model:

With the new and improved Ark Model 3000 — additional PPE capital arrives out of thin air! No need to finance capital intensive investments with debt or equity! For example, Keubiko put in $1,000,000,000,000.0 ($1T) in PPE and came out with an equity value per share of $11,000. Terrific news! If Telsa merely prints money like the US government and spends it on PPE, investors should be handsomely rewarded! Because the model fails to take into consideration how this PPE investment would be paid for, EBITDA rises in equally absurd proportions (see below):

In fact, not only does EBITDA skyrocket, total long term debt REDUCES with increased PPE investment. This type of modeling makes former Enron executives salivate. Unfortunately for ARK Invest, Keubiko wasn’t the only FinTwit user to shed light on this absurdity.

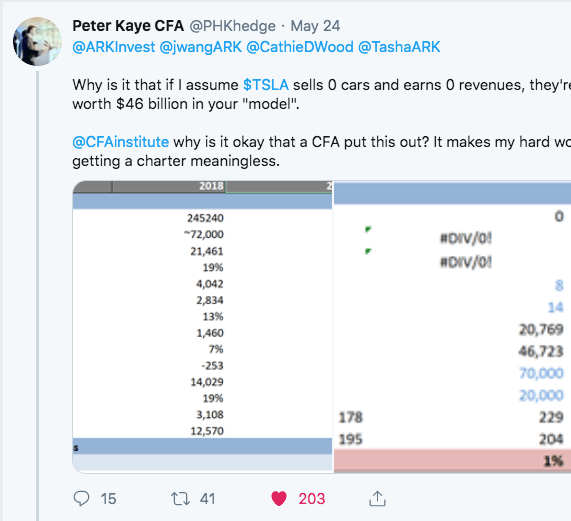

Peter Kaye, CFA — When Zero Revenues = $46B Valuation

Peter Kaye, CFA discovered that — within the model — if Tesla sold zero cars and generated zero dollars in revenues, the company would be worth $46B. That isn’t a typo — I didn’t mean to say $46. $46,000,000,000. This seems odd given the fact that Tesla can barely survive with their current level of output — yet in ARK’s model, dropping to zero output makes Tesla worth more than Fiat Chrysler ($20B):

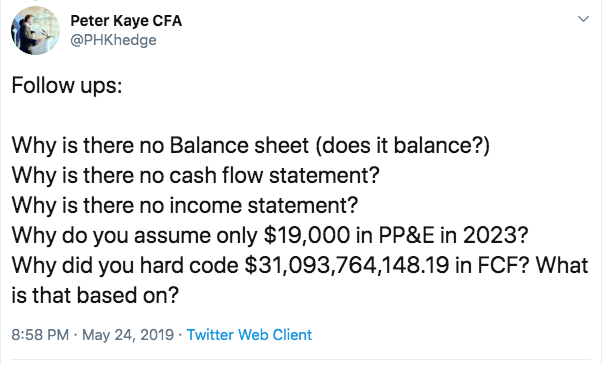

Peter goes on to mention a plethora of questions — good questions — regarding the model’s validity and inputs:

Why These Errors Matter

These are simply two examples of individuals that found erroneous judgements throughout this publicly released TSLA valuation model from Ark Invest. I’m sure there’s hundreds of others uncovering error after error related to this model, but these are the two that I found (YMMV). On a higher level, why does this matter? People make mistakes, we know that. But why did this valuation strike such a nerve within the FinTwit community? I think it had to do with three main factors: Tesla, the CFA Institute and Misrepresentation.

Tesla is without a doubt the most talked about company in the FinTwit universe. If this model was for another company I’m sure its errors would’ve been exposed at some point, but given the (mostly negative) popularity within the FinTwit community around the electric car company, I’m not surprised to see such a quick uncovering of errors.

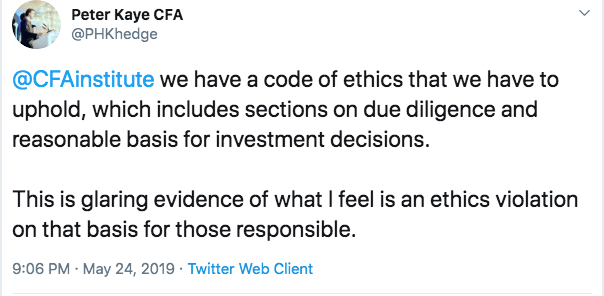

Peter Kaye loops the CFA Institute into the discussion, and I’m glad he did. Tasha Keeney of Ark Invest has her CFA charter. Peter claims that as a CFA, analysts should be held to higher standards than the work that Tasha released on Ark Invest’s behalf:

Peter’s case is strong for a violation based on reasonable basis for investment decisions and due diligence. The model seemed to be anything but reasonable (i.e., $1T PPE investment without any increase in debt or equity to finance).

All of these factors lead to what appears to be an attempt to misrepresent the valuation of Tesla. Formatting numbers to make it look like billons of dollars when its actually hard-coded in the thousands leaves a nasty taste in my mouth. Now maybe we give them the benefit of the doubt — maybe it was a true error that wasn’t meant to be. I don’t think that’s the case. If it was an honest mistake, we have yet to see an apology tweet from Tasha, Ark Invest or any related parties.

How We Can Prevent This: Honesty, Transparency and Simplicity

The first step is to be honest with yourself and with your community. For every modeling example like the one above, I have to remind myself that honest, transparent valuation exists out there. Take Aswath Damodaran’s philosophy of valuation — it’s about as honest as they come. He’s open about how his valuation is his alone, and others might come to different conclusions based on the differing stories they tell. It’s refreshing. Be honest with yourself and the community you serve.

Second, valuation needs to be logical and rational. Do not confuse that last sentence as me saying valuation needs to be “conservative” by definition — that’s not what I’m arguing. If you have an outrageously bullish outlook on a company, your numbers need to reflect that outlook — and they need to make logical sense. Do you expect a company to invest heavily in growth over the next 5 years? If so, we should see heavy reinvestment back into the business in your model. Do you expect PPE to ramp up? That’s fine — we need to see how that will be financed in the model. It’s not the story that’s the problem, it’s the misrepresentation of the numbers to justify the story that’s the problem.

Finally, great investment ideas should be explainable via back-of-the-envelope math. Mohnish Pabrai said in an interview that an idea, “should hit me over the head like a 2×4”. What he means by that is the idea should be so obvious to you that you can’t help but research further. If I’m worrying about the decimal place of cell Z45 on the third sheet of my 10-year DCF model, that idea is probably a bad idea! If an analyst has to adjust PPE to $19,000 instead of $19B and format the model so that PPE is financed out of thin air to arrive at a “bullish” equity value — it might not be the model that’s the issue but the underlying hypothesis. Simplify. Simplify. Simplify.

Concluding Remarks

I want to thank Peter Kaye CFA and Keubiko for their tremendous work at uncovering the flaws in the Ark Invest TSLA model. I want to stress that I’m not attacking Ark’s stance on TSLA and TSLA’s valuation — they’re completely entitled to their bullish opinion. What I cannot tolerate is the model’s blatant errors leading to such valuations. Hard-coding $19,000 while making it look like $19B is misleading. Increasing PP&E without drawing from equity or debt financing to fund such increases is erroneous. I’m thankful to the FinTwit community for calling out these errors.

I hope Ark Invest takes the critiques of the above Twitter users seriously and adjusts their model accordingly. I’m not rooting for anyone to fail, but rather to learn from what has happened and make sure it doesn’t happen again.