Corteva, Inc. (CTVA) is a leader in global seed and crop protection products. The company provides farmers with the right mix of seeds, crop protection and digital solutions to maximize yields and increase profitability. Their mission is to ensure an abundant food supply for the growing global population. Corteva is going public on Monday, June 3rd after its spin-off from DowDuPont (DWDP).

Like most spin-offs, Corteva could be mispriced by the market due to indiscriminate selling, lack of research or various “ick” factors on the balance sheet (i.e., lots of perceived debt). We can’t control how the share price trades once the company goes public, but we can control our definition of perceived intrinsic business value over the next five years. The thesis for Corteva is simple: Here’s a pure-play agriculture company leading its field in an industry with sustained long-term tailwinds, high free cash flow generation and a strong balance sheet. Through improved cost synergies, a robust product pipeline and shareholder-first capital allocation policy, CTVA has numerous levers to pull to expand multiples and margins. The company is expected to open around $27/share. We think this is a fair value for the business. We just hope we can get it for less.

The All-In-One Solution for Farmers

Corteva operates two main segments: Seed Development and Crop Protection. Through these segments the company creates a one-stop-shop for farmers across the globe — they capture the farmer at the point of seed selection as well as protection for their own seed (read: virtuous cycle).

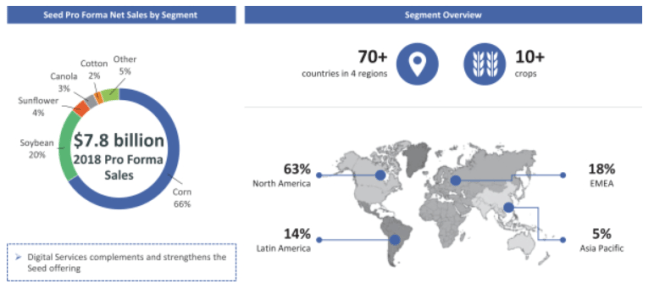

The seed development segment provides farmers with high quality germplasm coupled with patented trait technology to produce higher yields without increasing acreage. The company is the industry leader in many of the crops / geographies it sells. For example, Corteva’s seeds are either #1 or #2 in Latin America, Europe / Middle East – Africa, Asia Pacific and North America. More specifically, leading crops include corn, sunflower, soybean, alfalfa, sorghum, canola and winter wheat. These seeds produce higher yields through improved resistance to weather, disease and insects / weeds.

Source: Corteva Form 10

Crop Protection is much like its seed development brother — it leads almost anywhere it sells. Corteva offers protection products and services for over 100 crops in 140 countries. The protection products cover crops like wheat, corn, soybean, sunflower and canola. What exactly are the crops being protected from? Weeds, insect and nematode management, disease and nitrogen levels.

Source: Corteva Form 10

On a standalone basis, both segments produce high levels of EBITDA and healthy margins. Seed development generated $7.8B in revenues with $1.1B in operating EBITDA. Crop Production generated $6.4B in revenues with $1.1B in operating EBITDA (slightly higher margins). Combined the two segments generate over $14B in revenues and over $2B in EBITDA.

Industry Primed for Growth

Corteva is well positioned to capture the growth in the agriculture industry. The tailwinds are simple and can be looked at from a mathematical formula:

Increased population + increased global meat consumption = Need for increased food / crop production (read: Corteva)

We’re faced with two main challenges going forward. First, a rising global population puts sustained pressure on yields. Second, as more developing economies grow, the global middle class will rise, causing more individuals to consume more calories (meat consumption is positively correlated with GDP growth). These forces — which grow exponentially as populations rise — put stress on farmers to provide the highest yielding crops in the most space-efficient way possible.

From here, supply and demand forces will push the importance (and desirability) of investing in agriculture and AgroScience. You’re already starting to see this in movies if you look close enough. Most movie plots about the future involve some derivative of food shortage / agricultural issue. Management estimates growth rates for the agriculture industry to range between 2% – 4%. The company believes they’ll be able to grow about industry rates, somewhere between 3.5% – 6%.

Cost Cutting = Higher Margins

Generating incrementally higher revenues and EBITDA on new products isn’t a challenge for Corteva — those products offer higher prices, more technology and in turn better margins. On existing products, the company’s begun measuring at reducing headcount, improving synergies and using technology to expand margins.

Since the close of the merger Corteva’s slashed headcount by 4,000, consolidated 22 seed production facilities / 22 R&D sites, reduced commercial offices by 158 and shut down two non-performing crop protection manufacturing plants. These measures alone have accounted for over $800M in cost savings (from 2017 – current), 33% ahead of their initial goal. The company’s raised initial cost savings guidance from $1.1B to $1.2B by 2021 on a cumulative basis. Management believes these cost savings will add roughly $500M in additional operating EBITDA capacity (without doing anything on the product development side).

Effective & Efficient Capital Allocation

Higher margins, increased profits and cash flow are nice — but how does management intend on spending the cash? Dividends, buybacks and Growth investment. Corteva anticipates roughly $400M in dividends (targeting 30% of net income) with dividends increasing as net income and earnings rise. Management also expects to approve of a share repurchase plan at the time of spin-off for roughly $700M. Growth investment rounds out the capital allocation policy with around $2B — consisting of $1.2B in R&D, $100M in digital solutions and $400M in growth capex. These investments should provide the company with ROIC in the mid to high teens over the next five years.

Finding Our Roughly Right Valuation

We know the industry drivers are there, we know what kind of margins CTVA can generate — we also know where shares will start trading (around $27). But what we don’t know is how the next five years will play out. There are numerous risks in agriculture (which we’ll get to in a second), so creating a roughly right range given pessimistic, stagnant and optimistic views is crucial.

For our pessimistic view, we’re assuming -5% top-line growth, 15% margins each of the next five years and $4B in net debt. We’re assuming stagnant margins in our pessimistic view because the company’s grown margins each of the last three years. With our assumptions set, we arrive at 2023 revenues of $11B, $1.65B in EBITDA and $765M FCF. Average Enterprise Value (on an FCF basis and EBITDA multiple) comes in around $12B for an intrinsic value per share around $11-$12 (747M shares).

Our stagnant case assumes no top-line growth but return to margin expansion. Our 2023 revenues remain at $14.28B with $2.5B in EBITDA and $1.38B in FCF. We’re also going to assume that the company trades in line with its peer multiple (11.5x). With these figures in mind, we arrive at an Enterprise Value around $14.5B and intrinsic value per share around $20.

Finally, in our optimistic scenario we’re assuming management’s growth projections of 5% top-line, margin expansion towards 17% over the next five years and a slight premium multiple compared to its peers of 12x. Using these estimates and projections we end 2023 with a little over $18B in revenues, over $3B in EBITDA and $1.5B in FCF. Enterprise value comes in around $23B with intrinsic value per share a little over $25.

Risks: Seasonality, Debt (& Pensions) and Weather

There is a plethora of risks when dealing with agricultural companies — unfortunately us humans can’t really control the big one: weather. Last year the US corn belt suffered severe flooding. Flooding is dangerous because it washes away the crop protection products CTVA offers. This means that even if the crops survive the flood, they remain susceptible to disease, insects and weeds.

Another risk is the natural seasonality of the business. 80% of CTVA’s seed sales occur between the first and second quarters of the year. This means Corteva spends the first three quarters ramping up working capital — and a lot of debt. Although the company generates a significant amount of cash from these sales, they don’t collect that cash until the end of Q4. In other words, the company is a net user of cash 3 out of the 4 business quarters. This isn’t ideal in a business model, and it’s a risk we need to take seriously.

Finally let’s talk about debt and pensions. Given the seasonality in their business, Corteva normally ramps up debt levels towards $4B by Q3 before paying it off by the end of the year. Along with this seasonal debt, the company has historical DowDuPont pension plans on its books, which require annual payments of $200-$300M annually. These pension payments directly affect FCFF — resulting in lower cash flows over the course of the next five years. We should treat these as operating expenses and add them on to our capital expenditures when modeling out cash flows.

It’s Not Undervalued — Not Yet

At current share prices (around $27), I don’t think CTVA is undervalued. Rather at that price I would call it fairly priced. This means we’re faced with the dreaded questions: Do we pay a good price for a great business? Do we wait for the great business to offer a great price? I don’t know the right answer. What I do know is I would really like to buy shares for under $20. There are too many good opportunities out there to rush your entry price. Corteva has the chance to be a great opportunity — but only when the price allows.